Anthropic Just Fired a Warning Shot at the SPV Economy: Is the AI Gold Rush Headed Toward a Private Market Rug Pull?

Why Millions of Passive Investors's Retirement Accounts May Be Exposed to Private Market Structures They Don’t Actually Understand

For the last several years, millions of Americans have unknowingly moved deeper into one of the most opaque corners of modern finance.

Not through meme stocks.

Not through crypto speculation.

Not through day trading.

But quietly… through retirement accounts, alternative investment funds, wealth management platforms, pension allocations, and “exclusive access” private market opportunities sold under the banner of sophistication and diversification.

The average investor never saw it happening because the marketing language in the prospectus (that went unread) sounded reassuring. Their advisor liked it too because it had:

private equity exposure

late-stage venture access

pre-IPO opportunities

institutional-quality alternatives

AI innovation funds

diversified private growth

What most people never realized, is that many of these products were built on top of increasingly layered legal structures known as SPVs — Special Purpose Vehicles — that often created distance between the investor and the actual underlying asset they believed they owned.

Now, one of the most important AI companies in the world may have just exposed how fragile parts of that ecosystem really are.

And if the ripple effects spread, this story could eventually impact not just venture capital insiders but also retirees, small business owners, pension beneficiaries, and passive investors across the broader financial system who didn’t even know they had exposure to the asset class through this market structure.

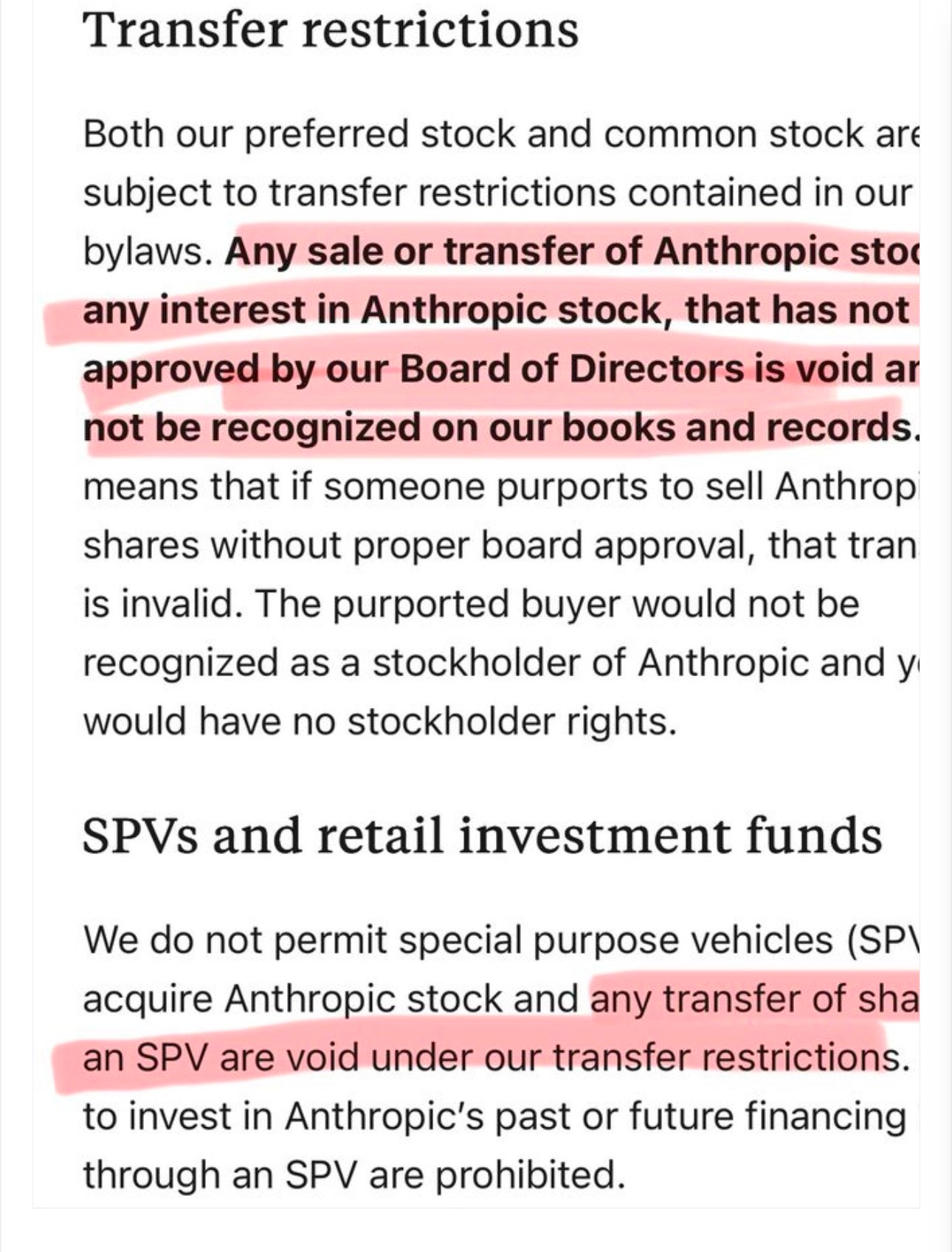

Here is the highlighted change in Anthropic’s terms that I believe could be a “shot heard around the world” as it relates to market structure.

The Warning Shot Few People Understand

Recently, Anthropic publicly clarified (see screenshot above) that unauthorized transfers of its stock are considered void unless approved by its board of directors. More importantly, the company explicitly stated that it does not permit SPVs to acquire Anthropic stock and that transfers involving SPVs violate its transfer restrictions.

At first glance, this sounds like legal housekeeping.

It is not.

It is a direct challenge to one of the fastest-growing trends in modern private alternative asset class investing:

”the retail-ization and syndication of access to elite private companies before they go public.”

For years, accredited investors and family offices who lacked direct venture capital relationships still wanted exposure to the fastest-growing private companies:

Anthropic

OpenAI

SpaceX

Stripe

Databricks

Anduril

Since, in recent years, these companies stayed private far longer than startups historically did, enormous wealth creation began happening before IPOs ever occurred. That created massive demand for secondary market access as both insiders (who wanted access to liquidity with each follow-on round before the IPO) and outside the venture loop investors wanted pre-IPO exposure.

And where demand exists, financial engineering follows.

What an SPV Actually Is

An SPV, or Special Purpose Vehicle, is not inherently dangerous. In fact, SPVs are used throughout legitimate finance every day. They are commonly used in:

real estate syndications

infrastructure projects

aircraft financing

venture capital

litigation funding

film production

tax planning

liability segregation

At its simplest level, an SPV is just a legal container for a pool of investor capital that keeps the cap table ledger clean for the deal with one shareholder. For example:

Imagine 200 investors all want exposure to one private AI company. The startup itself may not want 200 names added to its shareholder registry.

So instead:

A sponsor creates an LLC (SPV)

Investors buy membership interests in the LLC

The LLC purchases the shares.

This creates operational simplicity for the company. At least in theory. But here is where things become more complicated — and potentially dangerous.

The investors often do not directly own the startup shares. They own interests in the LLC (SPV). That distinction may sound technical.

It is not.

It may become the single most important detail in the entire structure, because exposure to an asset is fundamentally different from direct ownership and custody of the asset.

The Difference Between Ownership and Exposure

Most passive investors assume:

“If I (or my 401k, or pension fund, or IRA, etc.) invested in a SpaceX SPV, I own SpaceX stock.”

Legally, that may not be true.

Instead, the structure may look something like the SpaceX shares are held by:

a nominee

a fund manager

or the SPV itself.

The passive investor then owns:

units, interests, or contractual economic rights inside the SPV. NOT IN SpaceX stock directly.

Sometimes there are even additional layers:

feeder funds

offshore entities

transfer agreements

forward contracts

synthetic participation rights

The deeper the layering becomes, the farther the passive investor moves away from direct ownership and more counterparty risk is introduced for any potential claims or liens on that SpaceX stock.

And this means they become more dependent on

counterparties

managers

legal interpretations

liquidity events

and company approval.

Anthropic’s move effectively reminds the market of one critical reality:

Economic exposure is not the same thing as official stock ownership, as recognized by the company or its Board of Directors. In short, their ledger does not have to equal your ledger, and they are stating clearly who they think dictates who can hold the shares and transfer them to whom.

That distinction is suddenly becoming very important.