The $124 Trillion Wealth Transfer Will Create Winners, Losers, and Forced Sellers at Scale

Learn how the Great Wealth Transfer will expose every weak estate plan—and what you can do to preserve the wealth, avoid preventable loss, and position yourself to acquire what others cannot keep.

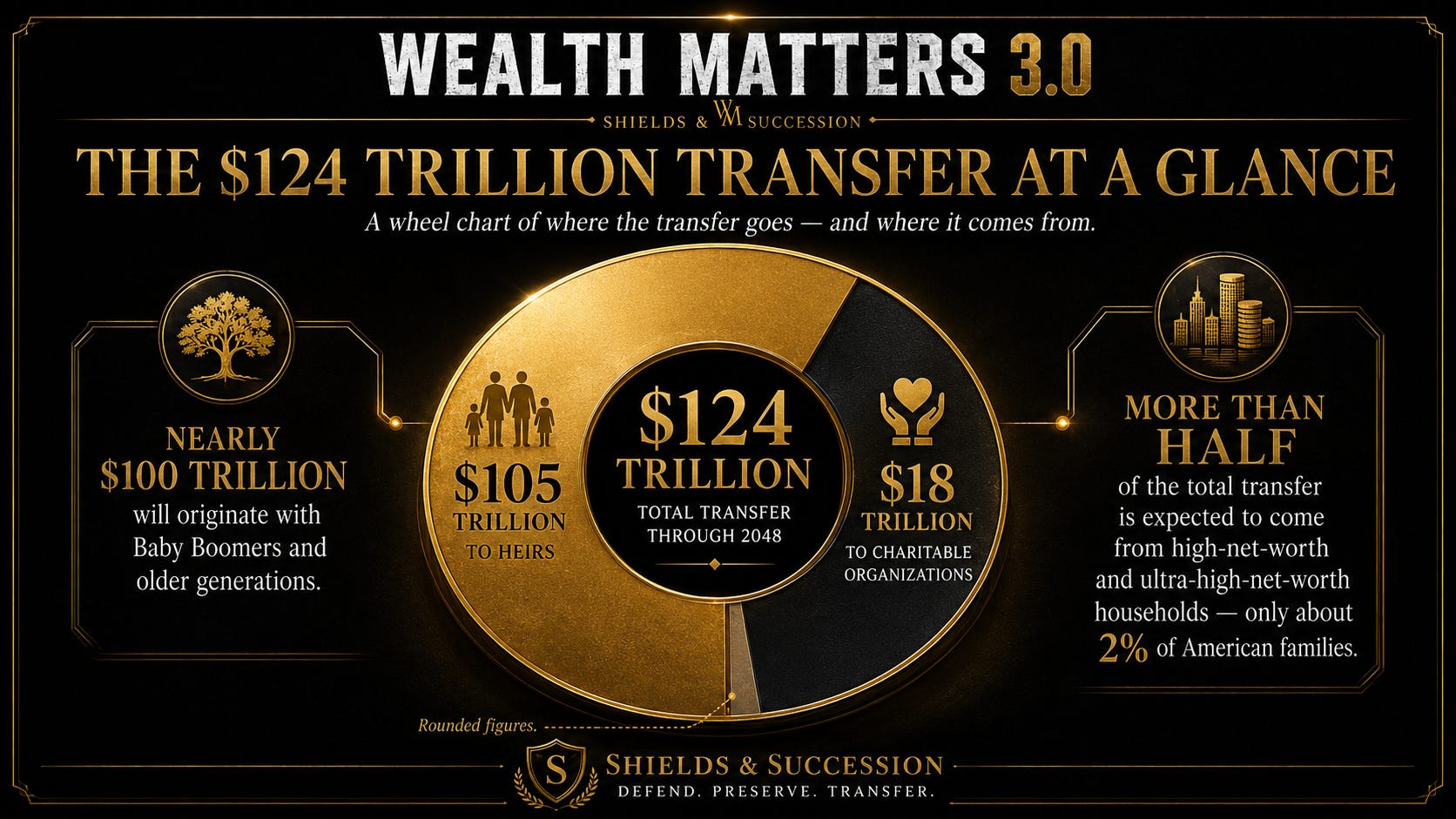

Cerulli Associates estimates that approximately $124 trillion will transfer through 2048.

About $105 trillion is expected to pass to heirs.

Roughly $18 trillion will be directed to charitable organizations.

Nearly $100 trillion will originate with Baby Boomers and older generations,

And more than half of the total transfer is expected to come from high-net-worth and ultra-high-net-worth households, which represent only about 2% of American families.

That is the headline data in a nutshell. But the headline conceals the more consequential story.

The Great Wealth Transfer is not a single transaction in which $124 trillion moves cleanly from one generation’s account into the next generation’s account. It is a decades-long migration of businesses, homes, commercial properties, securities, retirement accounts, mineral rights, insurance proceeds, partnership interests, collectibles, intellectual property, debt obligations, and family responsibilities.

At the current estimate, more than $5 trillion of wealth will change hands annually over the next 22 years through 2048.

Every dollar will have to pass through a gauntlet of documents, tax rules, family dynamics, health events, market conditions, professional fees, creditors, cybercriminals, government programs, and human judgment.

The gross transfer is approximately $124 trillion. The net legacy will be whatever survives the journey.

Every Estate Has a Gross Value and a Net Legacy

Most families think about inheritance in gross terms.

There is a house worth $2 million. A business worth $8 million. An investment portfolio worth $4 million. There may also be insurance policies, retirement accounts, private investments, and valuable personal property.

Add everything together, divide by the number of beneficiaries, and assume each person has a pro-rata share.

But a theoretical share is not the same as a protected share.

Before an asset becomes usable wealth in the hands of the next generation, someone must establish ownership, locate the documents, validate the beneficiary designations, settle liabilities, manage the tax consequences, maintain the property, resolve disputes, and decide whether the asset should be retained, refinanced, divided, or sold.

Every unresolved issue introduces friction. Every month of delay introduces cost.

Every forced decision introduces the possibility that a valuable asset will be sold at the wrong time, to the wrong buyer, for the wrong reason.

This is why families should stop asking only,

“How much are we worth?”

The more important question is:

How much of what we own is structurally capable of surviving us?

A family can be wealthy on paper and still be succession-poor. It can own millions of dollars of assets while lacking the liquidity, authority, records, governance, and decision-making capacity necessary to preserve those assets through a death, disability, or family conflict.

In those cases, the estate does not merely transfer. It leaks.

Leakage Is Larger Than Taxes

When people hear the word confiscation in an estate-planning conversation, they often think immediately about estate taxes.

Taxation is certainly relevant. Federal transfer taxes, state estate or inheritance taxes, capital-gains consequences, and property-tax reassessments can all affect what ultimately reaches the beneficiary.

But for many families, the greatest danger is not one dramatic tax bill. It is cumulative leakage.

Leakage can occur through avoidable taxes, probate expenses, professional fees, unresolved debts, deferred maintenance, insurance gaps, family litigation, creditor claims, poor investment decisions, and forced asset sales.

It can occur when no one has the authority to act during incapacity. It can occur when a family business loses customers, employees, or enterprise value while heirs argue about control. It can occur when children inherit equal ownership of an unequal burden.

Example:

One child may want to operate the business.

Another wants cash.

A third wants to retain the property for sentimental reasons.

The documents may divide ownership evenly without creating a mechanism for making decisions, financing a buyout, or resolving a deadlock.

The estate plan succeeded in transferring title, but it failed to transfer functional control. That distinction will define a meaningful portion of the $124 trillion transition.

The Incapacity Gap Comes Before the Inheritance

Much of the coming leakage will happen before death.

Cerulli projects that approximately $54 trillion will first move between spouses, with nearly $40 trillion expected to pass to widowed women in the Baby Boomer and older generations.

That means the Great Wealth Transfer is partly a story about inheritance—but it is also a story about aging, caregiving, widowhood, and the transfer of financial responsibility.

A surviving spouse may suddenly become responsible for an investment portfolio, operating company, commercial property, or network of professional relationships that the deceased spouse primarily managed.

The family may technically have a trust, a power of attorney, and a financial advisor. Yet the surviving spouse may not know where the documents are, why the investments were selected, who can be trusted, or which decisions require immediate attention.

Financial vulnerability also increases when cognitive capacity declines. Diminished financial capacity can leave an older adult more susceptible to financial abuse, impersonation schemes, unsuitable investments, and manipulation by relatives, caregivers, or supposed professionals.

The future estate can therefore be depleted years before anyone reads the will.

A modern succession plan must protect the owner not only from death, but from the period in which that person is alive, increasingly dependent, and potentially unable to defend the wealth independently.

Lawful Recovery Can Feel Like Confiscation When No One Planned for It

Another source of loss is long-term care.

Families frequently assume that Medicare, Medicaid, private insurance, or the eventual sale of a home will somehow resolve the financial consequences of extended care. The actual result depends on the individual’s health, assets, insurance, jurisdiction, and eligibility.

Federal rules generally require states to seek recovery from the estates of certain Medicaid recipients for specified long-term-care and related medical expenses, subject to protections and exceptions for qualifying survivors.

That is not arbitrary confiscation. It is a statutory recovery process connected to benefits previously provided.

But to an heir who believed the family home was protected, it can feel indistinguishable from a seizure.

This is an important distinction for Shields & Succession readers: an outcome does not need to be illegal or unfair to be devastating.

Many forms of estate leakage are entirely lawful.

Creditors may have legitimate claims. Taxes may be properly assessed. Medicaid recovery may be authorized. A fiduciary may have to sell an asset to pay expenses. A lender may enforce loan covenants. A minority partner may exercise rights granted under an agreement signed decades earlier.

The role of planning is not to pretend these obligations do not exist.

It is to understand them early enough that the family retains options.

Your Pro-Rata Share Is Not a Number. It Is a System.

A beneficiary may believe that one-third of a $9 million estate equals a $3 million inheritance.

It may not. One-third of an illiquid business is not $3 million in cash. One-third of a commercial property is not automatically financeable.

One-third of a concentrated stock position may carry substantial market and tax exposure.

One-third of a family vacation home may be an annual expense rather than an investable asset. One-third of an estate tied up in litigation may be inaccessible for years.

A protected pro-rata share requires more than favorable language in a will. It requires a functioning system connecting ownership, legal authority, liquidity, taxation, insurance, cybersecurity, investment management, and family decision-making.

The family needs to know what it owns, how it is titled, who controls it, what liabilities attach to it, and what event could force its sale.

The operating agreements must agree with the estate documents. The beneficiary designations must agree with the intended plan. The insurance must match the liabilities.

The successor trustee must be capable of doing the job.

The family must know who can act if the principal becomes incapacitated.

The heirs must understand which assets should be preserved and which can be sold without destroying the family’s long-term compounding engine.

These four elements are the difference between estate planning as document production and succession planning as an actively managed loss prevention strategy.

The Defensive Opportunity: Build the Shield Before the Event

The families most likely to preserve their share of the transfer will treat succession planning as an ongoing discipline rather than a one-time legal transaction.

They will maintain a current inventory of assets, debts, guarantees, digital accounts, insurance policies, and professional relationships.

They will examine how every meaningful asset would behave under death, disability, divorce, litigation, market stress, or the loss of a key operator.

They will create enough liquidity that valuable assets do not have to be sold merely because cash is needed to pay taxes, settle debts, maintain properties, or equalize inheritances.

They will establish governance before conflict arises. They will introduce spouses and adult children to the professionals responsible for the family’s wealth. They will prepare heirs not merely to receive capital, but to make decisions under pressure.

They will develop safeguards against unauthorized transfers, impersonation scams, compromised email accounts, and exploitation by people already inside the family’s circle of trust.

The shield is not a binder on a shelf. It is the coordinated ability to act before confusion becomes irreversible loss.

The Offensive Opportunity: Someone Will Buy the Assets That Others Cannot Keep

The same $124 trillion transfer also creates one of the largest asset-accumulation opportunities of the next quarter-century.

The next generation will not retain everything it inherits. Some heirs will receive properties they do not want to manage. Some will inherit minority interests in private companies they do not understand. Some will need immediate liquidity to pay taxes, settle debts, fund retirement, divide an estate, or buy out other beneficiaries. Some will inherit businesses without a qualified operator. Some will inherit land in one state while living and working in another. Some will inherit portfolios that are too concentrated, too complex, or inconsistent with their own priorities. Some will simply prefer cash.

The coming transfer will therefore create millions of motivated sellers—not necessarily because the underlying assets are poor, but because ownership has passed to someone for whom the asset is no longer useful.

This generational turnover may also collide with a broader reversal in the capital markets. For a much deeper look into the impact of this I encourage you to also read Ben Reinberg‘s recent piece this week in his Alliance Intelligence essay, “The End of the Passive Tailwind,” where he warns:

“The marginal buyer becomes the marginal seller. Do not assume the passive flood keeps flowing.” Ben Reinberg | Alliance Fund

That observation matters far beyond public equities, as it impacts hard assets like real estate, precious metals, crypto, Bitcoin, fine art, and auto collections, etc.

For decades, Baby Boomers and other working-age investors steadily contributed capital to retirement plans, brokerage accounts, funds, and passive investment vehicles. That recurring accumulation helped create a persistent bid beneath financial assets.

But aging eventually changes the direction of the flow. Contributors become withdrawers. Accumulators become distributors.

Owners who spent decades reinvesting earnings begin drawing income, funding care, simplifying estates, and liquidating assets that the next generation may not want to retain.

The Great Wealth Transfer is therefore not happening in isolation. It is unfolding at the same time that a historically wealthy generation is moving from accumulation into distribution.

The demographic cohort that helped supply the marginal bid may increasingly supply the marginal inventory.

That does not mean every inherited asset will be sold or that markets must decline mechanically. It means investors should not assume the capital flows that characterized the accumulation era will continue unchanged through the distribution era.

The assets reaching the market will not be limited to stocks and bonds. Commercial properties may be sold because heirs cannot agree on capital improvements. Family businesses may be sold because no successor wants to operate them. Partnership interests may be discounted because beneficiaries value liquidity over control.

Farmland, mineral rights, intellectual property, and private investments may become available because the new owners lack the expertise, interest, or patience to manage them.

The next generation of distressed assets may be created by succession, not recession. ~Chris J Snook

For prepared investors, this creates an opportunity to accumulate fundamentally sound assets from structurally unprepared ownership groups.

The prepared buyer will have capital, underwriting capacity, professional management, and the ability to close without adding more chaos to an already difficult transition.

That is opportunistic accumulation—but it should not be predatory accumulation. The best transactions will solve legitimate problems.

A well-capitalized buyer can provide liquidity to heirs, preserve jobs, improve neglected properties, recapitalize businesses, and place assets under more capable stewardship.

The opportunity is not to exploit grief. It is to be the rational counterparty when inherited complexity requires a solution.

The Best Offense and Defense Require the Same Capabilities

Interestingly, the qualities that protect a family’s existing wealth are the same qualities that allow an investor to accumulate assets from the transfer.

Liquidity.

Accurate information.

Clear authority.

Professional coordination.

Patience.

Speed when speed is required.

The family without liquidity becomes a forced seller.

The investor with liquidity becomes the preferred buyer.

The family without accurate records loses negotiating leverage.

The investor with disciplined underwriting can distinguish a difficult ownership transition from a genuinely impaired asset.

The family that waits until a death to establish decision-making authority loses time.

The investor with established acquisition criteria can act while others are still determining who has permission to sign.

This is why Shields & Succession cannot be separated from investment strategy. Succession planning is capital preservation for one side of the transaction and deal sourcing for the other.

Three favors before you finish reading.

Hit the ❤️. The algorithm is a slot machine, and hearts are quarters.

Hit the 🔄 restack. Somebody in your network is two weeks into the beach, watching loved ones age, wondering what they will have to manage through the inevitable years ahead. Get them a leg up and some peace of mind.

Hit 📤 share. You know exactly one person who needs to start the daily phone call before it’s too late. Send them the Interlude.

Drop a comment. Tell me your bucket-of-apples moment, the lesson somebody pointed at you before you were ten. I read every one, and I reply to the ones that make me laugh, make me think, or make me money. Preferably all three.

There Are Three Ways to Participate in the Transfer

Every reader is likely to encounter the $124 trillion transition in at least one of three roles. You may be an owner attempting to transfer assets. You may be an heir attempting to preserve them. You may be an investor positioned to acquire assets that other families cannot efficiently retain.

Many people will occupy all three roles at different times. You may inherit one asset while selling another. You may protect your family business while acquiring a business from an owner without a successor. You may receive a share of an estate and use that liquidity to purchase real property being sold by another estate.

The transfer is not a single conveyor belt moving assets from old to young. It is a vast reallocation system in which ownership, control, liquidity, and capability are being renegotiated.

Your position within it will depend less on your age than on your preparation.

Do Not Merely Ask What You Will Inherit

The Great Wealth Transfer invites the wrong question:

“How much will I receive?”

A better set of questions begins with what could prevent the wealth from arriving intact.

What portion of the family balance sheet is illiquid?

Which assets require active management?

What happens if the principal becomes incapacitated tomorrow?

Who has the authority to protect the accounts?

Which liabilities or personal guarantees could survive the owner?

Would the heirs retain the business, operate it, sell it or fight over it?

Could the estate satisfy its obligations without selling its best assets?

Who would buy those assets if the family were forced to sell

Then the investor should turn the lens outward.

Which assets in your market are likely to face generational turnover?

Which privately held businesses have aging owners without successors?

Which properties are likely to pass to geographically dispersed heirs?

Which partnerships will need liquidity, recapitalization or professional management?

Where can your capital solve a succession problem while acquiring an asset capable of compounding under better stewardship?

Cerulli’s $124 trillion estimate is often presented as a demographic milestone. It is more than that. It is a warning about preventable loss. It is a forecast of enormous financial friction. It is a potential reversal of the capital flows that defined the accumulation era. And it is a map of where assets will move when ownership, capability, and intention no longer remain aligned.

The families that prepare will convert gross wealth into net legacy. The investors who prepare will acquire assets from those who do not.

Everyone else will discover that being named in the documents is not the same as being protected by them. The Great Wealth Transfer will not simply reward those fortunate enough to inherit. It will reward those prepared enough to preserve—and disciplined enough to accumulate.

Bring Your Questions to Matt Chats

The risks discussed here are deeply personal. They involve aging parents, family businesses, homes, trusts, beneficiaries, long-term care, inherited responsibilities, and assets accumulated over a lifetime. The correct answer is rarely found in a generic checklist because every family has a different combination of ownership structures, relationships, liabilities, and intentions.

That is why we created Matt Chats, our weekly live ATOMIQ LEVEL AMA for the Shields & Succession community.

Join Chris J. Snook and Matt Meuli every Wednesday at 1:00 p.m. Eastern and bring your questions, concerns, and real-life succession scenarios into the conversation.

Ask us about protecting an anticipated inheritance from unnecessary leakage, preparing for the incapacity or death of a parent or spouse, reviewing trust funding and beneficiary designations, assessing long-term-care exposure, preserving family businesses and inherited properties, preventing conflict among beneficiaries, creating liquidity before a forced sale, and responsibly acquiring assets emerging from generational transitions.

You do not need to disclose private names, account values,, or sensitive family information. Bring the situation, the concern or the question that has been keeping you awake.

Join us live every Wednesday at 1:00 p.m. Eastern for ATOMIQ LEVEL AMA: “Matt Chats”.

Because the best time to identify the leak is before the transfer begins.

The real risk is doing nothing!

~Chris J Snook with Matt Meuli

Sources and Further Reading

Cerulli Associates — The Great Wealth Transfer

“Cerulli Anticipates $124 Trillion in Wealth Will Transfer Through 2048”

Cerulli projects that $124 trillion will transfer through 2048, including approximately $105 trillion passing to heirs and $18 trillion going to charitable organizations. The research also estimates that nearly $100 trillion will originate with Baby Boomers and older generations.

Cerulli Associates — Spousal and Widow Wealth Transfers

“$54 Trillion Will Transfer to Widows Through 2048; More Than 95% Will Go to Women”

Cerulli estimates that $54 trillion will initially move through inter-spousal transfers and that nearly $40 trillion will come under the control of widowed women from Baby Boomer and older generations.

Ben Reinberg and Alliance Intelligence

“The End of the Passive Tailwind”

Reinberg examines the demographic shift from capital accumulation to capital distribution and the potential consequences when an aging investor population moves from supplying the marginal bid to becoming a source of withdrawals and asset sales.

Consumer Financial Protection Bureau

“Planning for Diminished Capacity and Illness”

Guidance on organizing financial records, establishing trusted contacts, creating durable financial powers of attorney and protecting people experiencing diminished financial capacity from fraud or financial exploitation.

Centers for Medicare & Medicaid Services

Federal information explaining when states are required to pursue recovery from the estates of certain Medicaid recipients for specified long-term-care and related services, along with applicable survivor protections and hardship provisions.

Internal Revenue Service

“Frequently Asked Questions on Estate Taxes”

Federal guidance concerning estate-tax filing requirements, the applicable exclusion amount and related estate-tax administration.

Federal Trade Commission

“Top Scams Affecting Older Adults”

FTC information concerning fraud aimed at older Americans and the growing financial losses associated with scams targeting older adults.

“False Alarm, Real Scam: How Scammers Are Stealing Older Adults’ Life Savings”

FTC analysis of high-dollar government and business impersonation scams targeting older adults, including cases involving victims transferring substantial portions of their retirement savings.

DISCLAIMER: Shields & Succession is a Wealth Matters 3.0 digest by Chris J. Snook and Matt Meuli examining how families can defend their wealth, prepare successors, and prevent a lifetime of accumulated assets from being lost during moments of transition.

This article is educational and does not constitute individualized legal, tax, or investment advice. Estate, trust, Medicaid, creditor-protection, and tax rules vary by jurisdiction and personal circumstance. Consult qualified legal, tax, insurance, and financial professionals before acting.

Check out: https://www.removetheregime.com/ 🐸🐸🐸

Let's kick this shitshow down the road and get back to REAL life...