The 7 Things Keeping the 50+ Crowd Up at Night About Their Estate — And the 3 Costliest Common Mistakes In Your Current Plan

Shields & Succession Q3 Sentiment Report and Office Hours Launch

Where the True Fear Is and Isn’t In the Economy

We pulled the last quarter’s worth of survey data, search behavior, and the questions people are actually typing into Google and AI answer engines about getting their “affairs in order.” A clear pattern showed up — and it’s not the one most people expect.

The fear is real. The preparedness is not. And a surprising amount of the worry is pointed at a threat that, for most families, no longer exists.

Here’s what’s genuinely top of mind for Americans age 50 and up right now, what the data says, and where the real risk is hiding.

The 7 2026 Concerns Online Sentiment Revealed

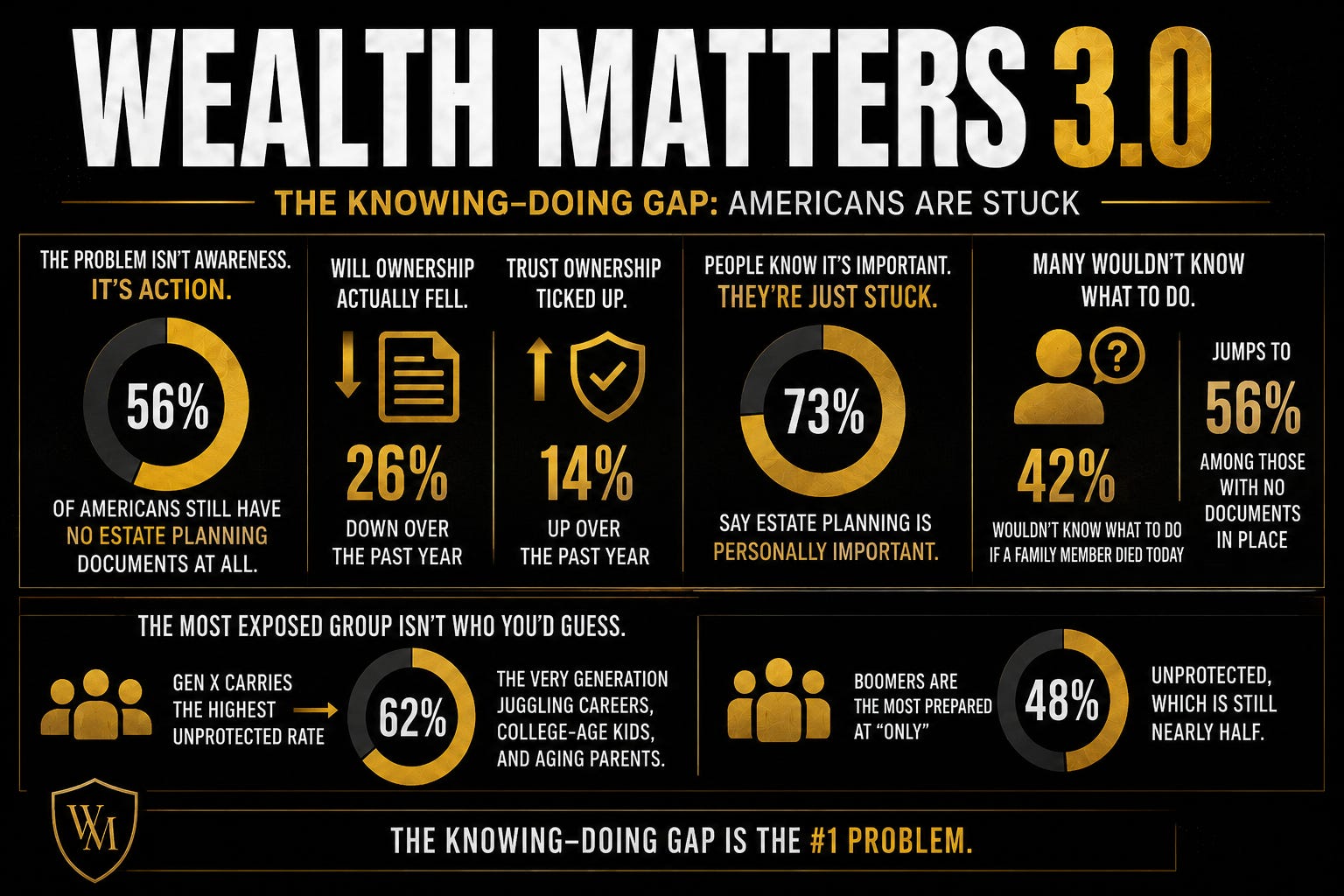

1. “I know I should, but I still haven’t.” The knowing–doing gap is the #1 problem.

The largest annual study in the space — Trust & Will’s 2026 report, drawn from 5,000 U.S. adults surveyed in late January and early February — landed on a number that hasn’t moved: 56% of Americans still have no estate planning documents at all. Will ownership actually fell over the past year, down to 26%, even as trust ownership ticked up to 14%.

The kicker: 73% say estate planning is personally important. People aren’t unconvinced. They’re stuck. And 42% admit they wouldn’t know what to do if a family member died today — a number that jumps to 56% among those with no documents in place.

The most exposed group isn’t who you’d guess. Gen X carries the highest unprotected rate at 62% — the very generation now juggling careers, college-age kids, and aging parents at the same time. Boomers are the most prepared at “only” 48% unprotected, which is still nearly half.

The real question isn’t whether you need a plan. It’s what’s actually stopping you from finishing the one you started.

This is exactly the kind of stuck point we work through live every week.

→ Save your free seat for this Wednesday’s Matt Chats — 1pm EST, live on Substack

2. “How do I talk to my parents about their money — without it getting weird?”

If you’re 50+, you’re often planning two estates at once: your own, and your aging parents’. This is the search query that’s quietly exploding — the “sandwich generation” money conversation.

The numbers explain the anxiety. A late-2025 Finance of America survey found that among self-identified sandwich caregivers, 86% feel emotionally exhausted, 80% physically exhausted, and 69% financially exhausted — all up sharply from 2022. Nearly a third expect a parent to eventually move in, and a third have already been asked to help cover a parent’s expenses. Allianz’s data echoes it: 70% say caregiving has significantly hit their own retirement plans, and 65% worry they won’t have enough to retire because of it.

The avoidance is understandable — nobody wants to look like they’re circling the inheritance. But the cost of not having the conversation is brutal: scrambling through a parent’s paperwork mid-crisis, discovering there was no plan, or learning too late that long-term care quietly drained the estate everyone assumed they’d inherit.

The fix is almost always a structured, low-pressure conversation before it’s urgent — covering where the documents are, who’s named to make decisions, and what the wishes actually are. It’s a skill, not a confrontation.

3. “What happens if I need long-term care — and who pays for it?”

This is the single most underestimated line item in retirement, and the search data shows people are finally waking up to it.

The sticker shock is severe. Based on the most recent Genworth/CareScout and A Place for Mom benchmarks, the national median runs roughly $70,800 a year for assisted living, about $78,000 a year for an in-home health aide, and north of $108,000–$127,000 a year for a private nursing-home room — with costs rising faster than inflation. The Center for Retirement Research at Boston College estimates a typical 65-year-old should earmark around $165,000 for future care needs (closer to $171,000 for women, who tend to live longer and need care longer).

Here’s the misconception that wrecks plans: Medicare does not cover long-term care. It covers up to about 100 days of skilled nursing after a hospital stay — and that’s it. Custodial care, assisted living, memory care, and ongoing in-home help fall outside it entirely.

That leaves three real funding paths: self-fund from savings, transfer the risk with long-term care insurance (premiums run roughly $1,500–$3,500 a year for a healthy 55-year-old), or structure for Medicaid eligibility, which has its own strict look-back rules and timing requirements that have to be planned years ahead, not in a crisis.

The shield here isn’t the policy. It’s deciding — on purpose, in advance — which of those three doors you’re walking through.

Ready to reach out to Matt’s firm directly for a human phone call?

Ask specific questions in condidence about your Life and Legacy or Wyoming Asset Protection Trust structure Pre-Consult Call (Human’s answer during office hours M-F 9 am-5 pm MST):

Colorado Residents Only Dial: (970)820-0090

Residents from All 50 States and territories dial: (307)463-3600