The Four Levers of This Fourth Turning Climax: Re-Contextualizing the Iran War, China, and Trump's Strategy.

Investor Memo, April 6, 2026 (Originally published internally)

Originally written March 30th, 2026, for my personal clients and internal team members. Published now to my Substack subscribers

Executive Premise

The clearest way to frame this thesis is that the struggle for AI-era hegemony is being decided by control over four strategic levers: two chokepoints, one reserve basin, and one settlement infrastructure. These are not abstract metaphors—they are the physical and financial systems that let intelligence scale into production, power, and exchange.

AI data-center electricity demand is projected to rise from about 415 TWh in 2024 to about 945 TWh by 2030. TSMC reached 69.9% of global foundry revenue in 2025. The Strait of Hormuz still carried about 20 million barrels per day in 2024, with 84% of crude and condensate flows moving to Asian markets. The U.S. imported only about 0.5 million barrels per day through Hormuz, equal to roughly 7% of U.S. crude imports and about 2% of U.S. petroleum liquids consumption.

This is why “three chokepoints” was close but not quite right. The more precise architecture is:

· Lever 1 (Chokepoint): Strait of Hormuz—the forward energy valve

· Lever 2 (Chokepoint): Taiwan—the frontier compute bottleneck

· Lever 3 (Reservoir): Western Hemisphere energy complex—the resilience buffer

· Lever 4 (Rail): Dollar settlement infrastructure—the transaction layer

Running through all four is a fifth reality: water is the biophysical constraint that limits compute, energy, and social order. This is not a separate lever but the hidden multiplier that magnifies every other strategic calculation.

What the Jiang framework adds is a wider macro lens: this war is not simply a regional military contest or a temporary oil shock, but the trigger for a broader global economic reorientation in which the cheap-energy assumptions that supported the last forty to fifty years of globalization are breaking down. The central sorting question becomes brutally simple: which nations depend on cheap imported energy and globally optimized trade routes, and which possess enough local or hemispheric resource depth to absorb the shock and reorganize faster than their rivals.

In that sense, the war’s significance extends beyond missiles, sanctions, and shipping lanes. It is exposing whether entire national development models were built on permanently available cheap energy, secure trade routes, and political confidence that can no longer be taken for granted.

I. The Fourth Turning Frame: Why This Moment Was Predictable

The 80-Year Cycle and the 2026 Resolution

In 1997, historians William Strauss and Neil Howe published The Fourth Turning, outlining a theory of cyclical history based on generational archetypes. Their central claim: American history moves in roughly 80 to 100-year cycles called saecula, each divided into four turnings that function as societal seasons.

The Fourth Turning is the crisis phase—a period of institutional collapse, public sacrifice, and existential threat that forces wholesale reorganization. Previous Fourth Turnings include the American Revolution (1773-1794), the Civil War (1860-1865), and the Great Depression through World War II (1929-1946).

The 2026 prediction:

Strauss and Howe made a specific temporal claim in 1997: “If the Crisis catalyst comes on schedule, around the year 2005, then the climax will be due around 2020, the resolution around 2026.”

The 2008 financial crisis served as the actual catalyst, close to their 2005 estimate. That places us precisely at the resolution boundary in 2026. Recent commentary from Neil Howe and broader analysis confirms we are in the climax-to-resolution transition, with institutional upheaval reaching maximum intensity.

The framework predicts:

· High catastrophe risk: Indirection, civil violence, geographic fracture, or authoritarian rule

· Technology of destruction escalates: Every Fourth Turning has seen an upward ratchet in destructive capability and willingness to use it

· Public sacrifice required: Individual freedom subordinated to collective survival

· Institutional death and rebirth: Old order collapses; new structures emerge

Why This Time Feels Different (But Isn’t)

The visceral sense worldwide that “something fundamental is breaking” is not recency bias. It is the lived experience of Winter, when institutional foundations fail simultaneously. Crisis-era politics do not optimize for efficiency—they optimize for survival, legitimacy, and control of essentials.

Investment implication: Markets systematically underprice paradigm shifts because most participants assume linear continuity. Fourth Turning climaxes destroy that assumption. The institutions, technologies, and power structures established during 2026-2028 will anchor the next 80 years.

II. The Four Levers in Detail

Lever 1: Hormuz—The Forward Energy Valve

The Strait of Hormuz is a 21-mile-wide passage connecting the Persian Gulf to the Gulf of Oman. It remains the world’s most important oil transit chokepoint, and its geopolitical value lies in asymmetry of exposure.

The numbers:

· Carried about 20 million barrels per day in 2024 (one-fifth of global petroleum liquids consumption)

· Over one-quarter of the global seaborne oil trade

· 83% of LNG through the strait went to Asia in 2024

Asymmetric exposure:

· 84% of crude and condensate through Hormuz flows to Asian markets

· China received approximately 40-50% of its imported oil from Gulf countries, relying on the strait

· U.S. imported only 0.5 million barrels per day through Hormuz (7% of U.S. crude imports, 2% of U.S. consumption)

Limited bypass capacity exists via Saudi and UAE pipelines (approximately 6.5 million barrels per day combined), but this covers only about one-third of strait transit volume. LNG has virtually no alternative routing.

Strategic implication: Any credible U.S. ability to shape, threaten, or secure flows through Hormuz disproportionately affects China and other Asian importers. In strategic terms, Iran matters not only because of proliferation or terrorism, but because the Strait of Hormuz is the highest-value external energy valve in the global system.

The Jiang lens strengthens this point by clarifying that Hormuz is not merely a route through which oil travels. It is the switch that can disable the cheap-energy premise underlying the export-led manufacturing systems of much of Asia. In that frame, the war does not simply raise prices; it destabilizes the production logic of economies built on importing Gulf energy and exporting manufactured goods into a global system designed around low input costs and reliable transport.

That is why the Strait matters beyond commodity markets. If cheap energy is no longer assumed, then the entire architecture of trade, industrial planning, and national competitiveness must be repriced around resilience, access, and exposure rather than around efficiency alone.

Lever 2: Taiwan—The Compute Bottleneck

Taiwan remains the decisive chokepoint for frontier compute because TSMC still dominates leading-edge foundry capacity. TSMC’s 69.9% global foundry revenue share in 2025 and Taiwan’s overall 70.2% IC industry share represent overwhelming concentration in a single geopolitical entity.

Why it matters:

· TSMC produces the majority of the world’s advanced AI chips

· Only source of sub-3nm chips at scale (required for frontier AI training and inference)

· Lead time for alternative foundry capacity: 5-10 years minimum at equivalent technology nodes

· U.S. domestic production (Arizona, Texas facilities) will not reach Taiwan capacity levels before 2030

U.S. export control architecture:

· Bureau of Industry and Security (BIS) maintains strict licensing for advanced AI chips to China

· January 2026 revisions to export review policy for computing commodities destined for China and Macau

· Controls extend to manufacturing equipment required for indigenous Chinese production

The Taiwan invasion calculation:

Any Chinese military action against Taiwan must account for immediate destruction or U.S. denial of TSMC facilities, a multi-year setback to Chinese AI development without access to advanced chips, and simultaneous energy pressure if Hormuz and Malacca are contested.

This is why Taiwan is not just a territorial dispute. It is the production bottleneck for the computational substrate of military power, industrial productivity, and AI leadership.

Lever 3: Western Hemisphere Reservoir—The Resilience Buffer

This is the piece that makes the broader thesis more persuasive and explains how the U.S. can sustain pressure at Hormuz without crippling itself.

Venezuela and strategic optionality:

Reuters reported U.S. military action in Venezuela in January 2026, with subsequent reports that Trump said U.S. oversight there could last years. EIA data confirms Venezuela holds about 303 billion barrels of proven crude reserves, the largest reserve base in the world.

Venezuela’s importance is more about reserves and strategic optionality than immediate barrels, because production capacity remains far below reserve potential due to decay, underinvestment, and sanctions. Even optimistic estimates put production near only 1.2 million barrels per day by end-2026.

Atlantic Basin and Latin American growth:

EIA says Brazil, Guyana, and Argentina are driving forecast crude growth in the region:

· Brazil: largest Latin American producer, scaling offshore pre-salt production

· Guyana: averaging about 750,000 barrels per day in 2025, expected to exceed 1.0 million barrels per day by 2027 as new Exxon-led projects start up

· Argentina: Vaca Muerta shale development adding unconventional supply

U.S. imports from Guyana rose to record levels in 2025, creating a new Atlantic Basin offshore source outside the Gulf.

Strategic implication:

This does not mean the U.S. “controls all Western Hemisphere oil,” which would overstate the case. The more defensible claim is that the Atlantic Basin and the Americas increasingly function as a reserve basin that improves U.S. resilience while Asia remains more exposed to Gulf transit risk.

The strategic picture is not that the U.S. becomes immune to Gulf disruption, but that the Americas increasingly provide a fallback energy basin. That rear-area security puts pressure on Iran, easier to sustain politically and economically than if Washington were equally vulnerable to Gulf flows.

This is where Jiang most clearly validates the reservoir concept. His argument is that the Western Hemisphere is unusually rich not only in oil and gas, but in food, fresh water, minerals, timber, and broad territorial depth, which means the United States sits inside a larger resource zone materially better positioned for a fractured world economy than the import-dependent manufacturing systems of Asia.

That does not erase U.S. financial or political vulnerabilities, but it does reinforce the memo’s central asymmetry: in a world reorganizing around secure access to resources rather than around frictionless globalization, the Americas function less like a peripheral supply zone and more like a civilizational rear base.

Lever 4: Dollar Rails—The Settlement Layer

The fourth lever is not a classic chokepoint. It is the possibility that Treasury-backed dollar stablecoin rails become the default settlement fabric for a 24/7/365 internet economy of humans, firms, and AI agents.

If that happens, U.S. power would not just sit in aircraft carriers, LNG terminals, and chip controls. It would also sit inside the default transaction architecture of digital commerce, where value clears instantly in dollar terms, and demand for U.S. sovereign collateral becomes embedded in machine-speed economic activity.

Why this extends hegemony:

A hegemon that wins the current crisis era and also succeeds in embedding its currency into the default transaction layer of internet commerce creates a self-reinforcing loop among demand for its debt, liquidity in its payment rails, and dependence on its legal-financial architecture.

That loop becomes more powerful in an AI economy because agents transact continuously, globally, and in tiny as well as large denominations. If those transactions settle in tokenized dollars backed by U.S. sovereign paper, then global demand for dollar collateral can deepen even as the form factor of money changes.

The 15-year extension thesis:

The contest for hegemony over the next 15 years may determine far more than the next cycle of great-power rivalry. If the United States preserves primacy through the current crisis era and successfully extends dollar dominance into AI-native payment rails through Treasury-backed stablecoin infrastructure, it could plausibly lock the dollar into the default settlement layer for a machine-speed digital civilization.

In that case, the winning power would not merely control energy chokepoints, semiconductor bottlenecks, and water-constrained compute infrastructure; it would also control the monetary rails through which the resulting digital economy clears value.

The limiting caveat:

Monetary dominance is never permanent by decree. Stablecoin rails can reinforce dollar demand, but they can also create new private chokepoints, invite regulatory fragmentation, and provoke rival sovereign payment architectures. The stronger claim, therefore, is not that U.S. supremacy would be guaranteed for a century, but that victory in the present crisis—combined with successful dollarization of internet-scale settlement—could materially lengthen the lifespan of U.S.-led order in a way most analysts still underestimate.

III. Water: The Constraint Beneath the Levers

Water is the original third chokepoint from earlier analysis, but in the final architecture, it functions as a meta-chokepoint—a cross-cutting biophysical constraint that conditions all four levers.

Why Water Cannot Be Omitted

Adaptation Intelligence’s core thesis, reinforced by Brookings, World Economic Forum, and regional water security research, is that AI is not merely compute-bound or power-bound; it is physically water-bound. In some regions, the issue is not temporary depletion but irreversible aquifer destruction through compaction once groundwater extraction outruns recharge.

This distinction matters because when groundwater extraction exceeds recharge deeply enough and fast enough, alluvial aquifers do not merely decline; their clay layers compact, pore space collapses, and the storage structure itself is destroyed on geological rather than political time. That means some AI-related water use is not creating a temporary shortage but burning through nonrenewable civilizational infrastructure.

Humans do not survive long without water, and AI does not scale without water either.

What Jiang adds here is not a technical hydrology argument so much as a systems argument. His treatment of the Gulf reinforces that energy, desalination, urban viability, imported labor, and investor confidence are all part of the same operating system, which means water stress in the region cannot be separated from geopolitical and financial fragility.

Data Center Water Consumption: The Hidden Multiplier

AI’s water demand is not confined to visible data-center cooling:

· A large data center can use roughly 300,000 gallons of water per day

· Some AI mega-campuses may draw millions of gallons daily

· The broader AI economy also consumes water through chip manufacturing and power generation, which can exceed data-center use itself

Regional projections:

· Middle East & Africa data center water consumption: 119.34 billion liters (2025) → 535.71 billion liters (2031)—an 870% projected increase.

· China data centers: 1.3 billion cubic meters (2024) → over 3 billion cubic meters (2030).

The 870% projected increase in cooling water usage compounds regional water stress, particularly in:

· Gulf Cooperation Council (GCC) states are building AI infrastructure in desert climates.

· Western and northern China provinces are already experiencing water stress.

· The U.S. Southwest is facing constraints affecting data center expansion plans.

Water as Force Multiplier Across All Four Levers

Water is what makes the energy lever sharper in the Gulf, because desalination is energy-intensive. Energy cutoff to Gulf desalination plants means urban water supplies (Dubai, Riyadh, Doha) are exhausted within 72 hours, creating existential legitimacy crises for regional governments.

Water underwrites the semiconductor lever because fabs require ultra-pure water in massive quantities. TSMC uses millions of gallons daily for chip production. Taiwan’s 2021 water crisis nearly disrupted semiconductor output, demonstrating vulnerability.

Water limits the resilience value of the Western Hemisphere reservoir because basin health matters as much as barrel count. Energy abundance does not solve aquifer depletion.

Water imposes a hard physical floor beneath the dream of frictionless digital settlement because autonomous commerce still runs on servers, grids, and cooling systems located in real watersheds.

Jiang’s account of the GCC’s vulnerability gives this section a sharper political economy edge. The Gulf’s great cities are not simply rich energy hubs; they are artificial urban systems maintained by desalination, imported supplies, foreign labor, cooling-intensive infrastructure, and above all, confidence that these places are permanently safe and functional. Once that confidence breaks, the economic damage can become nonlinear, because capital and talent do not wait for full systemic collapse before they leave.

Middle East Water Stress and the Iran Conflict Nexus

The Middle East represents the confluence of energy, water, and geopolitical pressure:

· Most water-stressed region globally: 16 of the 25 most water-stressed countries are in MENA

· Dependence on desalination: GCC states rely on energy-intensive desalination for freshwater

· Regional population growth: Jordan is projected to need multilateral water agreements plus domestic desalination just to meet 2035 population needs

In 2026, water has been identified as a “strategic weapon” and “threat to economic, political, social, and environmental stability” by leading risk assessment.

Control of Hormuz provides leverage over Middle Eastern water security through energy:

1. Gulf state desalination plants require a continuous energy supply

2. Disruption of energy imports = desalination shutdown = water crisis within days

3. Regional data centers dependent on water-intensive cooling systems

4. Populations in urban centers have less than 72-hour emergency water supplies

5. Energy cutoff creates cascading failure: no power → no desalination → no water → societal collapse

That is also why the Gulf may be more vulnerable economically than headline oil wealth implies. Jiang’s framing is that the GCC’s apparent permanence rests on a fragile fusion of energy revenues, American security guarantees, desalinated water, and global investor confidence, making it one of the clearest examples of how war can shatter not only infrastructure but the story a region tells about its own durability.

China’s Dual Water Vulnerabilities

Domestic data center water scarcity:

· China’s 4.3 million data center racks consumed 1.3 billion cubic meters in 2024

· Generative AI growth could see water usage surge dramatically

· Hydropower-dependent provinces (Sichuan, Yunnan) face “double whammy” of water and power risks

· Northern and western regions with data center concentration already water-stressed

Transboundary river dependencies:

· The Mekong River system affects the southern China industry and agriculture

· Brahmaputra River (shared with India) represents a potential leverage point

· Central Asian water agreements affect Belt and Road corridor stability

This dovetails with Jiang’s broader claim that China is among the least prepared major economies for a world of structurally expensive imported energy. His argument is that China’s legacy model depended on cheap energy in and manufactured goods out, while its hoped-for transition toward AI and innovation still remains energy-intensive, meaning water and power constraints are not side issues but direct constraints on the next development model itself.

Civilizational Implication

The most important implication is civilizational rather than merely industrial: populations cannot endure long without water, and regions that overbuild AI infrastructure on collapsing aquifers are not just making a bad utility decision but compounding political fragility.

In that sense, water is not ancillary to the Fourth Turning climax; it is one of the clearest signals that the next order will be determined by who best aligns financial ambition, technological buildout, and ecological reality.

IV. The Strategic Architecture: Iran and Venezuela in Context

Surface Justification vs. Deep Strategy

Official narrative: Nuclear nonproliferation (”no nukes for terrorists”), regional stability, protection of allies (Israel, Gulf states), counterterrorism.

Deep strategic calculus:

The Iran conflict serves as the mechanism to establish U.S. control over the Strait of Hormuz at the precise moment when:

1. AI computation becomes the primary driver of economic and military power

2. China approaches its Taiwan decision window (2027-2030 per DoD assessments)

3. Energy, chips, and water converge as interdependent constraints on AI supremacy

4. The U.S. maintains temporary advantages in all domains that may erode within a decade

Jiang’s game-theory framing also adds a useful caution here. He argues that strategic flexibility and escalation control can matter more than raw escalation dominance, and that Iran’s ability to target chokepoints and shape timing may create a more complex and costly conflict environment for the United States than a simple hierarchy-of-power model would imply.

That does not negate the memo’s leverage thesis, but it does strengthen the need for humility. A system can hold the stronger structural cards and still misplay them if it treats escalation as linear, predictable, and one-sided.

The Taiwan Deterrence Mechanism

Traditional deterrence: Direct military confrontation in the Taiwan Strait (high risk, uncertain outcome, massive casualties, potential nuclear escalation).

Four-lever deterrence architecture:

If China moves on Taiwan, the U.S. can:

1. Close Strait of Hormuz to China-bound energy shipments

2. Simultaneously blockade the Strait of Malacca (80% of China’s oil imports transit through Malacca)

3. Maintain semiconductor export controls (deny AI chip access)

4. Exploit water stress in Chinese data center provinces and industrial zones

Effect: China faces industrial collapse, AI development halt, domestic unrest, and energy starvation within 60-90 days—without direct U.S.-China kinetic conflict in the Taiwan Strait.

This is the “ultimate lever” thesis: Hormuz control, backed by Western Hemisphere energy resilience, allows the U.S. to defeat a Chinese Taiwan operation without firing a shot near Taiwan itself.

Venezuela’s Role: Rear-Area Energy Security

Venezuela does not replace Hormuz or solve all energy equations. Its role is more subtle: it creates strategic optionality and reduces U.S. vulnerability to any retaliatory energy squeeze.

With domestic U.S. production, Canada, and a rising Atlantic Basin supply arc (Brazil, Guyana, Argentina, potentially rehabilitated Venezuela), the U.S.-aligned system has greater buffer capacity. That makes it politically and economically easier for Washington to sustain Gulf pressure than if the U.S. were equally exposed to Hormuz disruption.

Venezuela is part of the enabling architecture that makes a Hormuz-centered coercive strategy more credible.

Timing: Why 2026 is the Climax

The strategic window for establishing chokepoint control is narrow and closing:

Convergence factors:

· AI infrastructure buildout: 2024-2030 represents a critical period for hyperscale data center deployment

· Taiwan semiconductor advantage window: U.S. domestic capacity will not reach parity until 2030+

· Chinese energy diversification is incomplete: Russia and Central Asia pipelines cannot yet replace Gulf volumes.

· Water stress acceleration: Climate impacts compound regional scarcity at an increasing rate.

· China’s military modernization: PLA capabilities for Taiwan operation are improving annually.

· Fourth Turning resolution: Strauss-Howe predicted the 2026 resolution phase.

This is not a coincidence. The Fourth Turning framework predicts that climax events involve “an upward ratchet in the technology of destruction.” AI represents exactly this: a technology so powerful that controlling its physical substrate becomes an existential imperative.

V. The Deal Structure: U.S.-China Trade in Context

Current State of Play (March 2026)

· Paris talks described as “remarkably stable”; farm goods, critical minerals, managed trade on agenda

· China signals willingness for new trade talks; demands U.S. scrap unilateral tariffs

· USTR simultaneously opens Section 301 investigations into structural overcapacity across manufacturing sectors

· U.S. maintains tightened semiconductor export controls; BIS revisions January 2026

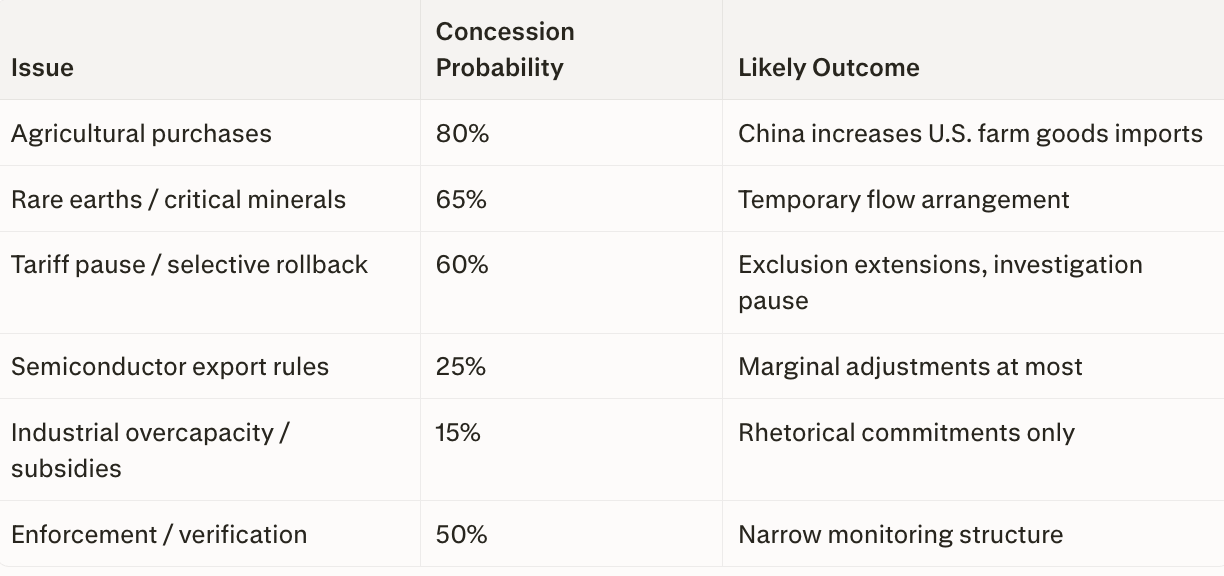

Deal Probability Assessment

Base case: 70% probability of a limited transactional deal

· Agricultural purchases (China buys more U.S. soybeans)

· Critical mineral flow arrangements

· Tariff pause or selective exclusion extensions

Alternative outcomes:

· 20% probability: No meaningful deal beyond rhetoric

· 10% probability: Broader structural settlement

Concession Probability by Issue

Who Needs a Deal More?

China faces greater pressure (65% of urgency):

· Youth unemployment: 16.1% in February 2026, jobs “hard to find”.

· Property crisis: Extended correction with “heavy price,” 17.2% YoY drop in December 2025.

· Social stability concerns: Regime sensitive to translating economic weakness into unrest.

· External trade stress compounds internal fragility.

U.S. pressure narrower (35% of urgency):

· Farmer constituency wants soybean exports restored.

· Market volatility from tariff uncertainty.

· Politically distributive pressure (can compensate affected sectors with fiscal support more easily).

Implication for investors:

The likely outcome is a tactical truce rather than a deep structural peace. China may offer near-term concessions (agricultural purchases, rare earth flows) to stabilize the situation, while the U.S. can afford to maintain long-term pressure on structural issues (chips, overcapacity, subsidies) that determine fundamental competitive position.

Both sides have reasons to avoid immediate escalation, but neither is prepared to concede on the core strategic contest.

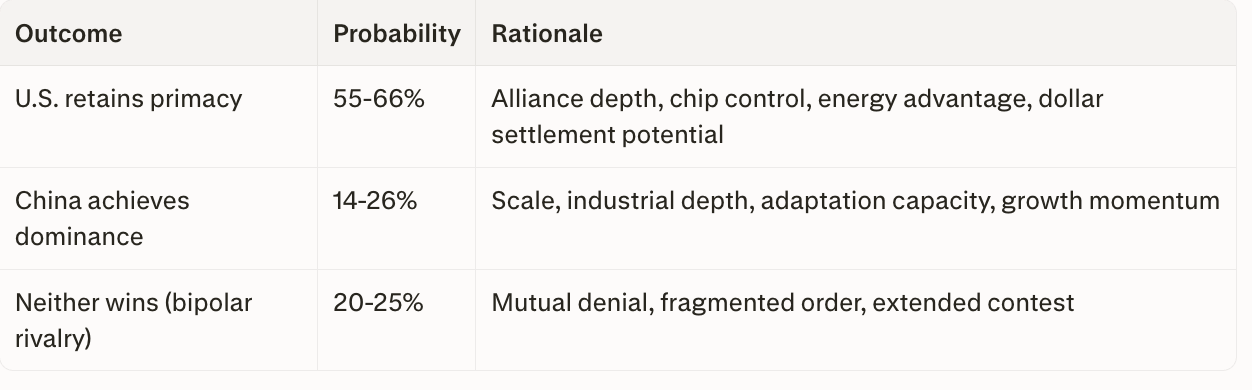

VI. Hegemonic Control Probability: The Next 15 Years

Base Case Assessment

Drawing on strategic positioning analysis, model ensemble reasoning, and current trajectory data:

Why the U.S. Leads

1. Military spending advantage: U.S. $997 billion (2024) vs China $314 billion; NATO allies committed to 5% GDP defense spending by 2035

2. Semiconductor chokepoint control: TSMC dominance + export control regime limits China’s access to frontier compute

3. Energy asymmetry: Hormuz disruption devastates China while the U.S. faces manageable stress; the Western Hemisphere buffer provides resilience

4. Alliance architecture: U.S.-aligned bloc represents a larger share of global GDP, technology capacity, and military power

5. Dollar settlement potential: If successfully embedded into AI-era transaction rails, it creates a compounding advantage

Why China Remains Dangerous

1. Economic scale and growth: IMF projects China 4.5% growth (2026) vs the U.S. 2.4%

2. Industrial depth: Manufacturing capacity and supply chain integration provide resilience

3. Military modernization: 7% defense budget increase (2026); improving Taiwan's operational capability

4. Adaptive capacity: Rapid renewable buildout, water efficiency investments, and alternative semiconductor development are progressing

The Decisive Variable

The contest will be determined by whether the U.S. can maintain its four-lever advantages long enough for the Fourth Turning resolution to crystallize a new institutional order that locks in American primacy.

Critical timeline:

· 2026-2028 (Resolution phase): Institutional structures for next saeculum established

· 2028-2030 (Early First Turning): New order stabilizes; late entrants face entrenched disadvantages

· 2030+ (New High): Pathway dependencies locked in for remainder of 80-year cycle

Investment thesis: Capital deployed during the 2026-2028 resolution window will benefit from 50+ years of structural tailwinds if positioned correctly. Capital deployed against the emerging order faces generational headwinds.

VII. Investment Framework: Positioning for the Resolution

The Crisis Climax Investment Principle

Fourth Turnings destroy old orders and create new ones. The last Fourth Turning climax (1940-1945) established:

· Bretton Woods monetary system (U.S. dollar hegemony)

· United Nations and international institutions

· Nuclear age and Cold War architecture

· U.S. industrial and technological dominance

· Social safety net expansion

These structures persisted for 80 years and generated incalculable wealth for investors positioned correctly.

The current resolution (2026-2030) will establish:

· AI infrastructure control regime (chips, energy, water)

· New monetary plumbing (digital currencies, payment rails)

· Reshored supply chains and regional blocs

· Reformed institutions or new governance structures

· Next generation of defense and security architecture

Sectors of Structural Advantage

Tier 1: Critical Infrastructure (Highest Conviction)

Advanced semiconductors:

· TSMC (Taiwan dominance, irreplaceable in medium term)

· ASML (only EUV lithography source)

· U.S. foundries (Intel, GlobalFoundries) if domestic buildout successful

· Chip design leaders (NVIDIA, AMD, Broadcom)

Energy infrastructure:

· U.S. LNG export terminals (Atlantic Basin advantage)

· Domestic oil and gas production (Permian Basin leaders)

· Nuclear power (next-generation SMRs, established utilities)

· Western Hemisphere energy exposure (Brazil, Guyana access)

Water infrastructure:

· Desalination technology providers

· Water recycling and treatment systems

· Smart water management and monitoring

· Industrial cooling solutions

Data center infrastructure:

· Hyperscale facilities in water-secure, energy-abundant regions

· Cooling technology providers

· Power infrastructure and grid modernization

· Data center REITs with strategic site selection

Tier 2: AI Value Chain (High Conviction)

Hyperscalers:

· Microsoft, Google, Amazon (AWS), Meta—own compute infrastructure and energy contracts

AI chip ecosystem:

· NVIDIA (dominant AI chip position)

· AMD (emerging alternative)

· Custom silicon teams (Google TPU, Amazon Graviton)

Vertical AI applications:

· Healthcare diagnostics and drug discovery

· Materials science and chemical engineering

· Defense and intelligence applications

· Financial services automation

Cybersecurity and infrastructure protection:

· Zero-trust architecture providers

· AI red-teaming and safety tools

· Supply chain security solutions

Tier 3: Reshoring and Supply Chain Security (Medium-High Conviction)

Domestic manufacturing:

· Automated factory systems

· U.S. industrial facilities

· Mexico nearshoring beneficiaries

Critical minerals:

· Domestic rare earth processing

· Lithium extraction and refining

· Graphite and battery materials

· Strategic mineral reserves

Defense industrial base:

· Munitions production

· Shipbuilding and aerospace

· Drones and autonomous systems

· Command, control, and communications

Tier 4: Monetary System and Hard Assets (Speculative but High-Impact)

Hard assets:

· Gold (monetary reset hedge)

· Bitcoin (digital scarcity, non-sovereign alternative)

· Real estate in water/energy-secure regions

New monetary infrastructure:

· Stablecoin issuers and infrastructure

· CBDC technology providers

· Payment rail modernization

Commodity producers:

· Energy producers (oil, gas, uranium)

· Agricultural producers in water-secure regions

· Water rights in advantaged geographies

Sectors of Structural Disadvantage

Assets likely to face generational headwinds:

· China-dependent supply chains: Firms with >30% China exposure without diversification plans

· Legacy institutions: Traditional media, established bureaucracies facing a legitimacy crisis

· Unsecured water infrastructure: Data centers and industrial facilities in water-stressed regions without mitigation strategies

· Long-duration sovereign bonds: Potential monetary reset creates duration risk

· Overleveraged commercial real estate: Credit availability contraction in a crisis intensification scenario

Portfolio Construction Principles

Core allocation (60-70%):

· Position in the foundational infrastructure of the emerging order

· Advanced semiconductor value chain

· U.S. energy infrastructure with Atlantic Basin exposure

· Hyperscale cloud providers with owned infrastructure

· Defense and cybersecurity prime contractors

Tactical allocation (20-30%):

· Water infrastructure and technology

· Critical minerals and strategic materials

· Reshoring and nearshoring beneficiaries

· AI vertical applications in strategic sectors

Optionality and hedges (10-20%):

· Hard assets (gold, Bitcoin, strategic real estate)

· Volatility instruments and tail risk hedges

· Emerging market exposure only in explicitly allied nations

· Short positions in legacy structures and China-dependent firms

VIII. Risk Factors and Counterarguments

Weaknesses in Our Four-Lever Thesis

1. Chinese Resilience and Adaptation

China has demonstrated capacity for rapid adjustment:

· Massive renewable energy buildout reduces fossil fuel dependency over time

· Investment in closed-loop water systems and efficiency technologies

· Alternative semiconductor development progressing (slower but real)

· Strategic petroleum reserves provide a 60-90 day buffer

· Alternative supply routes (Russia, Central Asia) partially mitigate Gulf dependence

2. Global Economic Interdependence

Four-lever warfare would devastate the global economy:

· Supply chain collapse across all industries

· U.S. allies (Japan, South Korea, Europe) were severely damaged

· Global recession/depression scenario

· Domestic political opposition to extreme economic warfare measures

3. Nuclear Escalation Risk

If China faces existential collapse from chokepoint strangulation, nuclear escalation risk increases:

· Rational deterrence suggests a cornered adversary is more likely to escalate

· Fourth Turning prediction: “upward ratchet in technology of destruction.”

· No historical precedent for a great power crisis with mutual nuclear arsenals

4. Water Scarcity Affects All Parties

Water is not a uniquely Chinese vulnerability:

· U.S. Southwest faces constraints affecting data center expansion plans

· The Taiwan semiconductor industry is vulnerable to drought (2021 water crisis precedent)

· Gulf allies face water crisis if energy is disrupted (potentially destabilizes U.S. regional position)

5. Dollar Rail Fragmentation Risk

Stablecoin-led dollarization could reinforce the dollar while dispersing value:

· Private issuers may capture value rather than the U.S. state

· Regulatory fragmentation creates alternative architectures

· Excessive weaponization accelerates search for alternatives

· China may develop parallel systems that fracture rather than displace the dollar

6. Fourth Turning Timing Uncertainty

While Strauss-Howe predictions have been accurate, the framework admits variability:

· Resolution could extend beyond 2026 into the late 2020s

· Crisis intensity varies (not all Fourth Turnings involve world wars)

· Generational boundaries are “erratic” per the authors

· Predictive frameworks can become self-fulfilling or self-negating

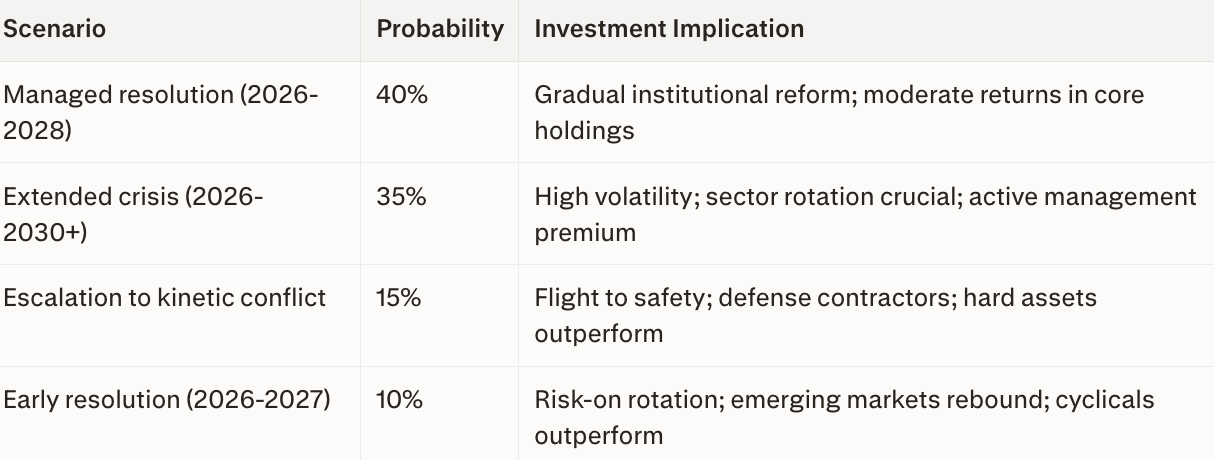

Scenario Analysis

Most likely outcome: Extended but ultimately managed crisis resolution spanning 2026-2030, with multiple escalation/de-escalation cycles creating high volatility but ultimately crystallizing a new U.S.-led order with embedded structural advantages.

IX. Synthesis: The Generational Mandate

What the Framework Tells Us

The convergence of Fourth Turning climax timing (2026 predicted resolution) with the strategic imperative to control AI infrastructure is not coincidental—it is the mechanism through which history’s cyclical pattern manifests in the age of computation.

Core insights:

1. Four levers determine AI supremacy: Hormuz (energy valve), Taiwan (compute bottleneck), Western Hemisphere (resilience reservoir), dollar rails (settlement layer)

2. Water is the hidden constraint: Limits all four levers; civilizational rather than merely industrial implications.

3. Asymmetric advantage favors U.S.: China is more vulnerable across energy, chips, water; U.S. has reserve depth.

4. 2026 is the climax year: Institutional structures established now persist for 50+ years

5. Trade deals will be tactical, not strategic: China needs near-term stabilization; the U.S. maintains long-term pressure on fundamentals.

6. U.S. primacy more likely than Chinese dominance: 55-66% probability U.S. retains system leadership.

7. Dollar settlement rail extension: Could plausibly lengthen U.S.-led order beyond normal 15-year cycle.

8. Resolution window is narrow: 2026-2028 represents a generational capital allocation opportunity.

For Investors: The Decisive Moment

The last Fourth Turning climax (1940-1945) established structures that persisted for 80 years and generated incalculable wealth for those positioned correctly at the institutional birth.

We stand at an equivalent moment.

The institutions, technologies, power structures, and monetary systems established during 2026-2028 will anchor the next saeculum. Pathway dependencies formed now will compound for decades.

Capital allocation mandate:

· Invest in the foundational infrastructure of the emerging order

· Avoid legacy structures facing obsolescence

· Accept higher volatility during transition in exchange for multi-decade structural tailwinds

· Position ahead of the resolution, not after it crystallizes

The Most Dangerous Scenario

The greatest risk is not successful four-lever control by the U.S., nor successful Chinese counter-adaptation, but rather partial implementation that backs a nuclear-armed adversary into a corner without acceptable off-ramps.

The Fourth Turning warns: “Every Fourth Turning has registered an upward ratchet in the technology of destruction, and in mankind’s willingness to use it.”

A cornered nuclear-armed China facing economic collapse, domestic instability, and loss of Taiwan without any face-saving exit is precisely the scenario that makes catastrophic escalation most likely.

Any strategy predicated on chokepoint dominance must include equally sophisticated escalation management and conflict termination planning.

The Greatest Opportunity

Crises, while terrifying, are also generative. The institutions, technologies, and power structures established during resolution phases anchor prosperity for generations.

Those who understand the pattern can position themselves for:

· Multi-decade structural tailwinds in strategic infrastructure

· Monetary system reset that embeds dollar dominance into new rails

· Regional and bloc-based trade creating long-term winners

· AI-era value creation concentrated in water/energy/chip-advantaged geographies

· Defense and security spending sustained at elevated levels for decades

This is not the end of history. It is the beginning of a new cycle—and those who understand the pattern will thrive in it.

X. Conclusion: The Resolution Ahead

We stand at the intersection of generational theory and geopolitical reality. The Fourth Turning framework predicted that 2026 would mark the resolution phase of an 80-year crisis cycle. Simultaneously, the race for AI supremacy has elevated control of physical and financial infrastructure to existential importance.

The Iran conflict, Venezuela intervention, Taiwan tensions, and U.S.-China trade confrontation are not separate events. They are the integrated manifestation of a contest for control over four strategic levers: the energy valve at Hormuz, the compute bottleneck at Taiwan, the reserve basin in the Western Hemisphere, and the settlement rails of the digital economy. Water runs through all of them as the biophysical constraint that makes everything else possible—or impossible.

What Jiang adds to this conclusion is the recognition that the war is functioning as a country-by-country sorting mechanism. Economies built on cheap imported energy, globally optimized supply chains, and confidence-sensitive urban systems are being forced into painful adjustment. In contrast, economies with deeper domestic or hemispheric access to food, water, energy, and logistics gain time, leverage, and optionality in the transition.

What happens in the next 24-36 months will shape the next 80 years.

Investors who recognize this convergence can position for generational wealth creation. Those who dismiss it as geopolitical noise or cling to the institutional structures of the dying order will face capital destruction as the old system collapses.

The memo’s final claim is calibrated and defensible:

If the U.S. wins or retains hegemony in the current crisis era and successfully embeds Treasury-backed dollar stablecoin rails into the default transaction architecture of the AI economy, it could plausibly create the conditions for a much longer-lived U.S.-led order than most observers currently price.

That is not a guarantee of a century of uncontested dominance. It is a recognition that victory in this Fourth Turning climax, combined with structural control over the four levers that enable AI-era production and exchange, creates pathway dependencies and compounding advantages that extend well beyond normal geopolitical forecast horizons.

The strongest synthesis, then, is this: the conflict is not merely repricing oil, but repricing entire national development models. Cheap energy, frictionless globalization, desalinated desert finance, and efficiency-first supply chains are no longer neutral background assumptions; they are now strategic variables that determine who can adapt, who can endure, and who can lead the next order.

Position accordingly. We are living through incredibly historic times.

~Chris J Snook

References and Endnotes

1. U.S. Energy Information Administration. (2026, March 25). “Amid regional conflict, the Strait of Hormuz remains a critical oil chokepoint.” EIA Today in Energy.

2. S&P Global. (2025, April 9). “Global data center power demand to double by 2030 on AI surge: IEA.”

3. Nature. (2025, April 10). “Data centres will use twice as much energy by 2030 — driven by AI.”

4. Focus Taiwan / market reporting. (2026, March 12). “TSMC rides AI wave to net nearly 70% of global foundry market in 2025.”

5. Morgan Lewis. (2026, January 15). “BIS Revises Export Review Policy for Advanced AI Chips Destined for China and Macau.”

6. U.S. Bureau of Industry and Security. (2026, January 12). Semiconductor licensing policy revision.

7. Reuters. (2026, January 8). “US Senate votes to curb military action in Venezuela, Trump says US oversight could last years.”

8. U.S. Energy Information Administration. (2026, March). “Venezuela country analysis/oil production.”

9. U.S. Energy Information Administration. (2026, March 25). “Brazil, Guyana, and Argentina support forecast crude oil growth in 2026.”

10. Brookings Institution. (2026, March 8). “AI, data centers, and water.”

11. Bloomberg. (2026, February 20). “Water Is Still Too Much of an Afterthought for Data Centers.”

12. Mordor Intelligence. (2024, December 12). “Middle East & Africa Data Center Water Consumption Market Report 2025-2031.”

13. China Water Risk. (2025, July 2). “China's ICT running dry? The rise of AI & climate risks amplify existing water risks faced by thirsty data centres.”

14. Adaptation Intelligence / Substack. (2026, March 15). Water security and AI infrastructure analysis.

15. Strauss, W., & Howe, N. (1997). The Fourth Turning: An American Prophecy. Broadway Books.

16. Konvergent Wealth. (2020, October 20). “The Fourth Turning – Did Neil Howe and William Strauss predict the crisis of 2020?”

17. Neil Howe interview. (2025, May 16). “The Fourth Turning is Here | Neil Howe Explains What Comes Next.” YouTube.

18. Podcast Notes / Art of Manliness. (2023, July 26). “The Fourth Turning — How History’s Crisis Period Could Unfold.”

19. Reuters. (2026, March 15). “US, China discuss farm goods, managed trade in ‘remarkably stable’ Paris talks.”

20. Reuters. (2026, February 24). “China says it will decide on US tariff countermeasures in due course.”

21. USTR. (2026, March 10). “USTR Initiates Section 301 Investigations Relating to Structural Excess Capacity.”

22. USTR. (2026, March 11). Fact sheet on Section 301 investigations into structural practices.

23. Reuters. (2026, March 17). “China’s February youth jobless rate dips to 16.1%.”

24. Reuters. (2026, March 15). “China’s economy builds early momentum in 2026 as global risks loom.”

25. Reuters Breakingviews. (2026, March 9). “China’s property reset comes with a heavy price.”

26. SIPRI Yearbook. (2025). Military expenditure data and analysis.

27. NATO. (2025, December 17). “Defence expenditures and NATO’s 5% commitment.”

28. IMF. (2026, January 18). “World Economic Outlook Update, January 2026.”

29. Goldman Sachs. (2025, November 20). “China’s economy is forecast to grow faster than expected in 2026.”

30. Carnegie Endowment for International Peace. (2024, April 18). “The Looming Climate and Water Crisis in the Middle East and North Africa.”

31. The Simplified Jiang. (2026, March 31). “What This War Means For Every Economy On Earth — Explained Country By Country | Prof Jiang Analysis.” YouTube. AI-presented explainer based on the ideas and analysis of Professor Jiang Xueqin.

32. Roya News. (2026, March 11). “A lesson in predictive history: Professor Jiang on why the U.S. will likely lose to Iran.” Summary of Jiang Xueqin’s lecture on escalation control, strategic flexibility, and the Strait of Hormuz.

End of Memo

Disclaimer:

This document is intended for institutional investors, family offices, and strategic advisory purposes. Views expressed are those of the author and do not constitute investment advice. Conduct independent due diligence before making investment decisions.

Furthermore, this memorandum is provided for informational and educational purposes only and does not constitute, and should not be construed as, individualized investment advice, legal advice, tax advice, accounting advice, or a recommendation to buy, sell, or hold any security, digital asset, commodity, derivative, or other financial instrument. The views and opinions expressed herein are those of the author as of the date indicated and are subject to change at any time without notice.

Wealth Matters Media, LLC; Chris J Snook; ATOMIQ; and any of their respective parents, subsidiaries, related or affiliated entities, managers, members, officers, directors, employees, contractors, agents, representatives, and any present or future affiliates (collectively, the “Affiliated Parties”) make no representation or warranty, express or implied, as to the accuracy, completeness, timeliness, or suitability of any information contained in this document. All information is provided on an “as is” and “as available” basis and may be based on third-party sources believed to be reliable at the time of writing; however, the Affiliated Parties do not independently verify such information and assume no responsibility for any errors, omissions, or resulting outcomes.

Nothing in this memorandum takes into account the specific investment objectives, financial situation, risk tolerance, or particular needs of any individual person or entity. Any examples, scenarios, probabilities, forward‑looking statements, or illustrative allocations are purely hypothetical, are provided solely for discussion purposes, and are not guarantees of future performance or outcomes. Actual results may differ materially from any views or scenario analysis expressed herein. Past performance is not indicative of, and does not guarantee, future results.

You are solely responsible for your own investment, financial, tax, and legal decisions. Before making any investment or implementing any strategy discussed in this memorandum, you should conduct your own independent research and due diligence and consult with qualified professionals, including but not limited to a registered investment adviser, broker‑dealer, attorney, and/or tax advisor, who can consider your individual circumstances. The Affiliated Parties are not acting as your fiduciary, investment adviser, or agent, and no advisory, client, or other professional relationship is created by your receipt of or reliance upon this document.

To the fullest extent permitted by applicable law, the Affiliated Parties expressly disclaim any and all liability for any direct, indirect, incidental, consequential, special, exemplary, punitive, or other damages, losses, or costs (including, without limitation, lost profits, trading losses, or opportunity costs) arising out of or in any way connected with (a) the use of or reliance on this memorandum or any information contained herein, or (b) any errors, inaccuracies, or omissions in such information, regardless of the form of action or theory of liability, even if advised of the possibility of such damages.

This memorandum is not, and should not be construed as, an offer to sell or a solicitation of an offer to buy any security or other financial instrument, nor is it intended to form the primary basis of any investment decision. Any references to specific companies, securities, instruments, sectors, geographies, strategies, or technologies are purely illustrative and do not constitute endorsements, recommendations, or solicitations of any kind. Any discussion of regulatory, geopolitical, or macroeconomic developments reflects a subjective interpretation as of the date of writing and may become inaccurate or incomplete without notice.

By reading this memorandum, you acknowledge and agree that: (i) you are solely responsible for any use you make of the information contained herein; (ii) you will not rely on this memorandum as the sole or primary basis for any investment or strategic decision; and (iii) you will hold harmless and release the Affiliated Parties from any and all claims, demands, causes of action, damages, losses, liabilities, costs, and expenses arising out of or relating to your access to, reliance upon, or use of this memorandum or any information contained herein.