Gratitude for a great conversation!

Before you read the show notes below,

Please subscribe to Roger

And get Roger’s book, The Ledger: How Important Assets Go Astray and a Framework for Sovereign Wealth

Roger’s conversation is a masterclass in practical understanding of what truly drives a nation’s (or family’s) wealth. His work is built around one of the most important but under-discussed questions in economics, politics, investing, and national stewardship:

What if GDP is only the income statement, and the real story is hiding on the balance sheet?

TL;DR Key Takeaways

Roger Ohan began his career in engineering, realized he did not like engineering, earned an MBA, and then entered finance through Chemical Bank, now JPMorgan Chase.

He was placed into a then-obscure corner of the market called fixed income derivatives and became one of the early traders in interest rate swaps, helping build part of what became JPMorgan’s core fixed income business in Europe.

Roger’s worldview was shaped by both extremes of finance: highly liquid, high-volume fixed income markets where billions could move in seconds, and illiquid emerging market equities where assets could trade once a month or once a quarter.

After leaving trading in 1997, he helped build an emerging markets asset management business focused heavily on Russian equities during the privatization boom, including exposure to the extraordinary rise and political destruction surrounding Yukos.

The seed of The Ledger began with a question that bothered him after Hurricane Katrina in 2005: how could a city be destroyed, families lose homes, businesses, memories, and assets, and yet the economic statistics fail to show the destruction of real wealth?

Roger’s core insight is that GDP measures flow, like an income statement, but it does not properly measure the condition of a country’s balance sheet.

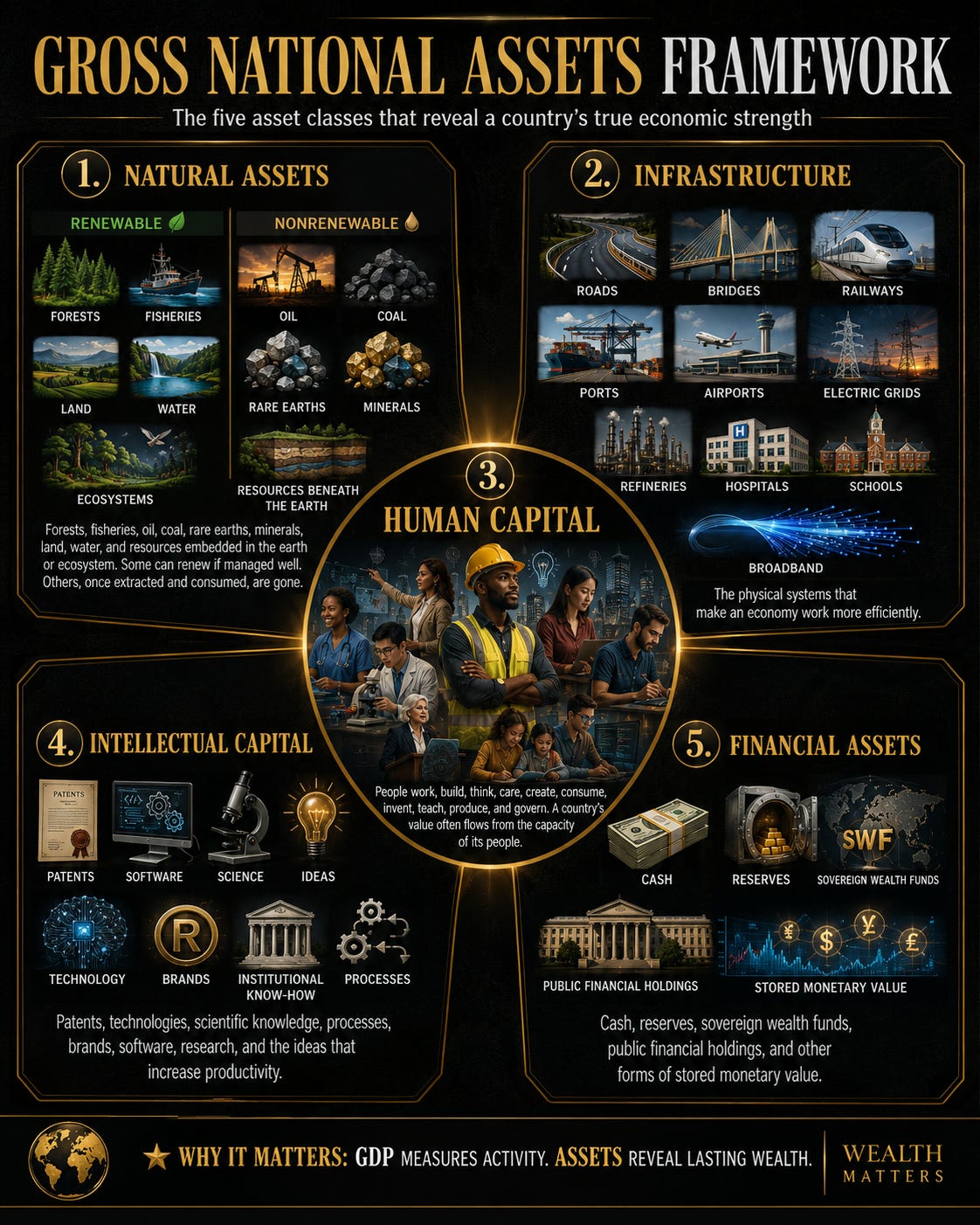

His Gross National Assets framework looks at five categories of national assets: natural resources, infrastructure, human capital, intellectual capital, and financial assets.

Those assets must then be weighed against liabilities, including debt, unfunded promises, deteriorating infrastructure, depleted resources, and future obligations.

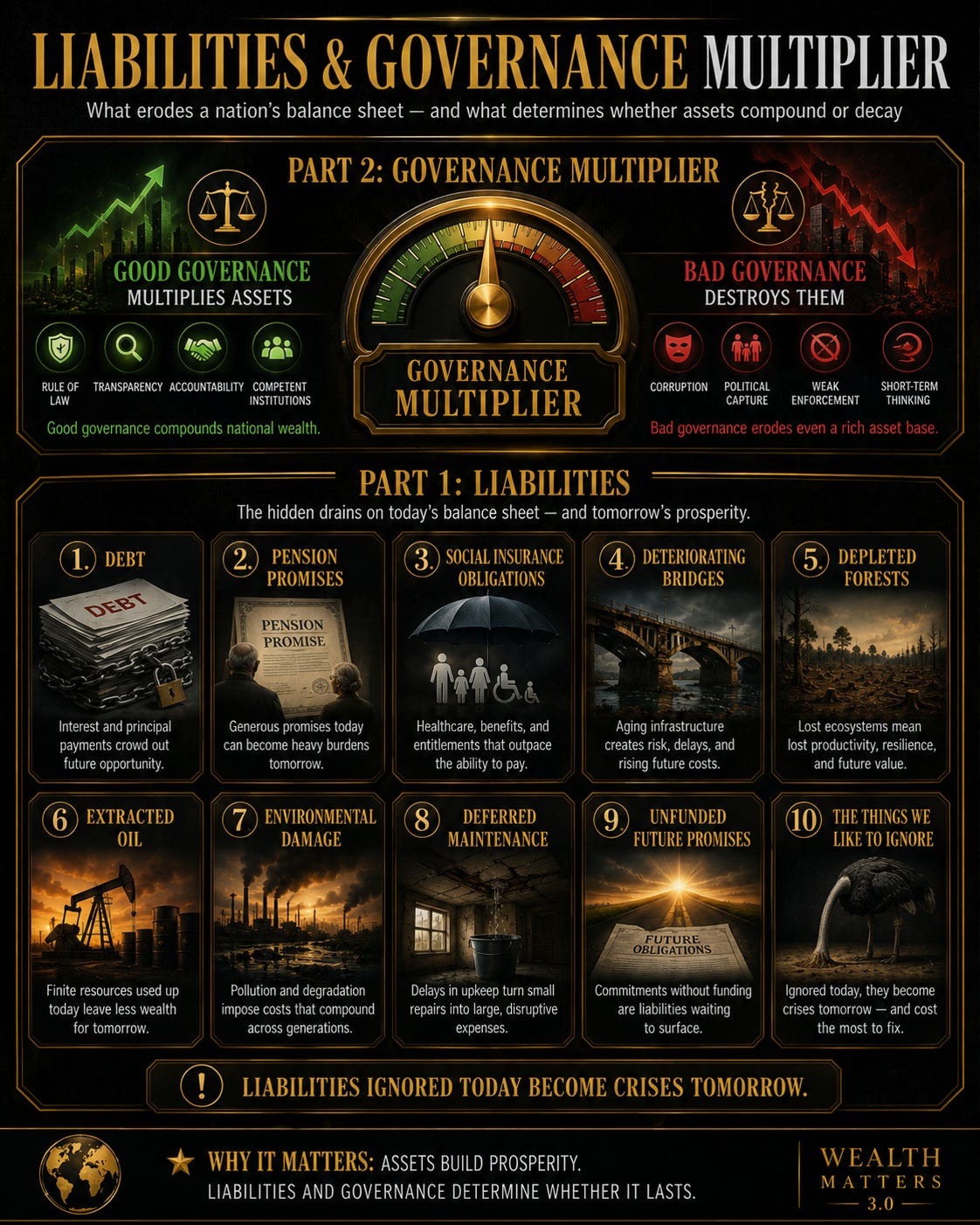

Over those assets sits what Roger calls the governance multiplier. Good governance compounds national wealth. Bad governance can destroy the same asset base.

The contrast between Norway and Nigeria is central to his framework. Both had oil. Norway converted its natural resources into a financial asset through a sovereign wealth fund and strong governance. Nigeria largely failed to convert its oil wealth into a durable national balance sheet strength.

Nauru is Roger’s cautionary tale. Once one of the richest countries in the world per capita because of phosphate deposits created by ancient bird guano, it mined its balance sheet, spent the proceeds poorly, and collapsed after the resource declined.

Singapore and South Korea are the positive examples. Both began with very little, especially South Korea after the Korean War and Singapore after separation from Malaysia, but built enormous sovereign wealth by investing in human capital, infrastructure, rule of law, and governance.

Cuba is one of Roger’s most striking examples of trapped human capital: a country with literacy, doctors, engineers, and education, but a governance structure that forces talent into low-productivity survival behaviors rather than compounding national wealth.

The framework introduces the “sovereign share,” the value of a country’s net assets divided by its population. In simple terms, it asks: how much national equity does each citizen effectively inherit?

AI complicates the framework because human capital is the largest balance sheet asset in advanced economies. If AI reduces the value of human labor faster than new productive roles emerge, national balance sheets may weaken in ways GDP will not immediately reveal.

Roger’s framework applies to families, business owners, and investors, too. Income matters, but the balance sheet matters more. A high-earning person or nation can still become fragile if they consume everything and fail to compound assets.

The deeper message: nations, businesses, and families should stop confusing activity with wealth creation.

Why You Should Listen

This ATOMIQ LEVEL conversation with Roger Ohan is not just a macroeconomics interview. It is the story of a man who spent decades inside the machinery of global finance, watching markets move in real time, watching countries rise and fall on governance choices, watching assets be created, extracted, wasted, or compounded, and finally deciding that the way we measure national prosperity is dangerously incomplete.

It is about a trader who began in the obscure world of interest rate swaps before they became central to modern finance, then moved into emerging market asset management, Russian equities, infrastructure advisory, fund administration, private equity restructurings, and board-level investment work.

It is about the moment Hurricane Katrina exposed something that GDP could not explain: the destruction of real human, physical, and financial wealth hiding beneath a headline economic metric that could still look superficially fine.

It is about why a car crash, a burned house, a ghost city, an unused bridge, a depleted island, and a mismanaged oil field can all increase measured economic activity while making the owner, the city, the country, or the people poorer.

It is about why Norway became one of the great sovereign wealth stories in modern history while other oil-rich nations burned through their balance sheets.

It is about why Singapore and South Korea prove that human capital, governance, education, rule of law, infrastructure, and patience can turn poor nations into extraordinary compounding machines.

It is about why the AI revolution may force us to rethink the value of human capital on national balance sheets, especially if brains, not just hands, are now being augmented or replaced.

Most of all, this conversation is about truth in accounting. Not the accounting of a company. The accounting of civilization.

Press play on this conversation with Roger Ohan, author of The Ledger, if you want a framework that helps you see through economic gaslighting, political scorekeeping, distorted GDP narratives, and the dangerous habit of confusing spending with wealth creation.

Because a nation can look busy and still be getting poorer.

A business can have revenue and still be eroding its future.

A family can have income and still fail to build a balance sheet.

And once you learn to see the ledger, you never look at prosperity the same way again.

The Man Who Looked Past GDP and Found the Missing Ledger

Gross National Assets and the Balance Sheet of Civilization

Before Roger Ohan wrote The Ledger, before he began developing the Gross National Assets framework, before he started asking whether countries were actually getting richer or merely producing activity that looked like growth, he was an engineer who did not want to be an engineer.

So he did what many smart people do when the first track does not quite fit.

He got an MBA.

Then he walked into finance through a bank called Chemical Bank, which would eventually become JPMorgan Chase. He did not begin in some obvious center of glamour. He was placed into a strange and obscure corner of the market that almost did not exist yet: fixed income derivatives. Interest rate swaps.

At the time, that was not the sprawling, central, institutional market it would later become. It was still emerging, still being built, still not entirely understood by the broader financial world. Roger was early. He was lucky, as he says, but he was also capable enough to understand what luck had handed him.

He became one of the early people trading swaps and helped build part of what became JPMorgan’s core fixed income business in Europe.

That is not a small thing.

It meant sitting in markets where every second mattered. Government bonds, repos, swaps, massive positions, payroll numbers, GDP releases, interest rates, and billions of dollars of exposure moved across screens in real time. A number would hit, and within seconds, markets would respond.

You could win or lose millions before most people even understood what had happened.

That kind of early career leaves a permanent mark. It trains a person to respect flows, liquidity, reflexes, leverage, and the brutal honesty of price. It also teaches a lesson most people outside markets never fully internalize:

The number everyone is watching may not be the number that matters.

The Dumbbell Life of a Market Thinker

Roger’s career did not stay on one side of the financial world. After years in highly liquid fixed income markets, he moved into the opposite environment: emerging market equities.

That shift gave him what he calls a dumbbell background.

On one side, there were some of the most liquid instruments in the world, moving constantly, reacting instantly, and repricing by the second.

On the other side, there were deeply illiquid emerging market securities, including Russian equities, where options might trade once a month or once a quarter.

One world was all speed. The other was all opacity.

Both taught him something.

From fixed income, he learned how the global monetary machine moves. From emerging markets, he learned what happens when governance, property rights, incentives, and state power sit underneath the numbers. He saw assets that looked cheap because they were cheap, and assets that looked cheap because the market did not trust the system around them.

One of the defining examples was Russia in the late 1990s, during the privatization boom. Roger was investing in Russian equities from roughly 1997 to 2000, a period when assets under management could go from zero to $500 million and then back down to $30 million because that was what Russian equities did.

They boomed. They collapsed.

They revealed the balance sheet and the governance structure at the same time.

Yukos and the Lesson of Governance

One of the stories Roger tells is about Yukos, once one of the most valuable oil companies in the world. At the time, the company was being treated like a cash register by its owner, Mikhail Khodorkovsky. Money was being pulled out. The market assigned the company a low value because governance was weak, and outside investors had no reason to trust that the asset base would be treated properly.

Then came a different idea.

Instead of extracting value from the company in the short term, leave the money in. Clean up the accounts. Use IFRS statements. Make the company transparent. Turn it from one of the dirtiest companies in Russia, financially speaking, into one of the cleanest.

The value skyrocketed.

That story matters because it shows one of Roger’s central insights long before he wrote the book. The asset was already there. The oil existed. The company existed. The productive base existed. What changed was governance.

The market did not merely pay for the asset. It paid for the trust in the asset.

Then Khodorkovsky took on Vladimir Putin. Putin decided the company was no longer really his. Khodorkovsky ended up in exile, and the story became another lesson in the same ledger.

Assets do not exist in a vacuum. They exist inside power structures. And when governance breaks, value can disappear.

The Moment Katrina Broke the Metric

The idea behind The Ledger did not arrive all at once. It accumulated over decades. But one moment crystallized it for Roger: Hurricane Katrina in 2005.

New Orleans was devastated. People died. Families lost homes. Businesses were destroyed. Generations of memories disappeared. Photo albums, which Roger notes may matter even more than the physical structure of a house, were gone. Local wealth, civic wealth, emotional wealth, human wealth, and physical wealth were wiped out.

Then the economic numbers came in. And they did not tell the truth.

That was the problem.

GDP could reflect the rebuilding activity. It could count the spending. It could capture the contractors, materials, repairs, and money changing hands. But it did not properly show the destruction of the balance sheet.

A city could be devastated, and the number could still fail to reveal the real loss.

That bothered Roger. It should bother all of us. Because once you see it in Katrina, you begin to see it everywhere.

The Car Crash That Explains the Economy

Roger uses a simple example to explain the flaw.

Imagine you own a $100,000 car. You crash it. The repair costs $10,000. You pay the mechanic. The mechanic is $10,000 richer. You are $10,000 poorer. Between the two of you, the money moved from one pocket to another.

But GDP records $10,000 of economic activity.

The problem is that your balance sheet is worse. Your cash is down. Your car may still be worth less than it was before the crash, even after the repair. The accident history may impair the value. The asset was damaged, and the repair did not necessarily restore the whole loss.

The economy looks more active. You are poorer. That is the central illusion.

Now scale that up. A house burns down. A hurricane destroys a city. A bridge is built where nobody needs it. A ghost city rises in China and then gets demolished. A country extracts oil or phosphate from the ground and spends the proceeds without replacing the asset.

GDP may count the work. The ledger asks whether wealth was actually created.

GDP Is the Income Statement

Roger is careful not to dismiss GDP entirely. GDP is useful. It was built for a purpose. It emerged during the Depression as a way to measure economic flow, and it became extraordinarily useful during World War II and the Cold War for understanding production capacity and how much of the economy could be shifted toward war, defense, or other priorities.

GDP does what it was designed to do. But it was never meant to do everything. GDP is the income statement. Roger wants us to look at the balance sheet.

That distinction is everything. A company can have revenue and still be fragile. A family can have a large income and still be broke. A country can show growth while destroying the very assets that make future prosperity possible.

Once you understand that, the economic conversation changes. You no longer ask only, “How much activity happened this quarter?”

You ask, “What happened to the asset base?”

Gross National Assets

Roger’s Gross National Assets framework begins with five major categories of assets.

The first is natural assets: forests, fisheries, oil, coal, rare earths, minerals, land, water, and the resources embedded in the earth or ecosystem. Some are renewable if managed properly. A forest can be perpetual if replanted and maintained. Oil, once pulled from the ground and burned, is gone.

The second is infrastructure: roads, bridges, railways, ports, airports, grids, refineries, hospitals, schools, broadband, and the physical systems that allow an economy to function more efficiently.

The third is human capital, which Roger argues is usually the most important asset in a country. People work, build, think, care, create, consume, invent, teach, produce, and govern. The value of a country is often downstream of the capacity of its people.

The fourth is intellectual capital: patents, technologies, scientific knowledge, processes, brands, institutional know-how, software, research, and the ideas that make the economy more productive.

The fifth is financial assets: cash, reserves, sovereign wealth funds, public financial holdings, and other forms of stored monetary value.

Against these assets sit liabilities.

Debt. Pension promises. Social insurance obligations. Deteriorating bridges. Depleted forests. Extracted oil. Environmental damage. Deferred maintenance. Unfunded future promises. The things we like to ignore until they become impossible to ignore.

Then, over the top of all of this, Roger places the governance multiplier. Good governance multiplies assets. Bad governance destroys them.

Norway, Nigeria, and the Governance Multiplier

The contrast between Norway and Nigeria is one of Roger’s clearest examples. Both had oil. That is the starting point. The natural asset existed in both places. But the outcome was radically different.

Norway created one of the world’s great sovereign wealth funds. It put rules in place before the oil money became irresistible. It designed the fund to be perpetual. It restricted what politicians could do with it. It converted a natural asset, oil in the ground, into a financial asset that could benefit future generations.

The governance framework protected the balance sheet.

Nigeria had enormous oil wealth too, but much of that wealth did not become durable national capital. It did not compound through human development, infrastructure, institutional strength, or broad-based financial assets in the same way. The oil came out of the ground, but the national balance sheet did not strengthen proportionately.

The difference was not the existence of oil. The difference was governance.

That is why Roger’s framework is not merely economic. It is civilizational. It asks whether a country has the institutional discipline to convert temporary resource wealth into permanent national strength.

The Island Made of Money That Became a Prison

Then there is Nauru.

Most people could not find it on a map. Roger says even after writing about it, he would struggle to put his finger within 500 miles of it on a globe. It is a tiny island in the Pacific Ocean, and at one point, it was one of the richest countries in the world per capita.

Why?

Birds.

For millions of years, birds nested there. Their droppings became phosphate deposits, valuable as fertilizer. The island was, in a very literal sense, made of money.

So Nauru mined it. It exported the phosphate. It spent the money. Citizens enjoyed benefits. The country looked rich. GDP looked impressive. But the country was consuming its balance sheet. The asset was being dug out and shipped away.

Then the quality of the phosphate declined. The revenue stopped. The balance sheet was gone.

Today, Nauru survives in part through arrangements such as serving as a detention location for asylum seekers intercepted by Australia.

That is the cautionary tale.

A country can be rich on paper while it is liquidating itself.

Singapore and South Korea: Starting From Nearly Nothing

If Nauru is the warning, Singapore and South Korea are the inspiration.

Singapore began with almost nothing. When it separated from Malaysia, it did not have abundant natural resources or vast land. Its people were poor. Its future was not guaranteed. But the government invested in human capital, rule of law, infrastructure, institutional credibility, and governance.

It made itself a place where people could trust the system. That trust became an asset.

South Korea’s story is equally powerful. After the Korean War, the country was devastated. It had little infrastructure, little financial capital, limited natural resource wealth, and a population that had to be educated and developed over generations. It invested in people, factories, universities, engineers, companies, and national capability.

Today, the world carries Samsung phones and drives Korean cars. That was not an accident. It was the balance sheet construction.

Singapore and South Korea show that a country can begin with very little and still create enormous wealth if it compounds human capital, infrastructure, intellectual capital, and governance over time.

That is the positive side of Roger’s ledger.

Cuba and the Tragedy of Trapped Human Capital

Cuba becomes one of the most haunting examples because it shows that human capital can exist and still fail to compound.

Roger points out that Cuba has high literacy, a strong base of doctors, a healthcare system with real human skill, and even specialized talent like nuclear engineers. Yet the country remains poor. Why? Because the governance structure does not allow those assets to become fully productive.

A doctor can make more in the tourism economy from tips than from practicing medicine under the official system. Highly educated people are pushed into survival behaviors rather than compounding the value of their education.

That is balance sheet destruction in human form. The asset exists. The system traps it.

This is what makes Roger’s framework so powerful. It does not simply ask whether a country has resources or educated people. It asks whether the system allows those assets to generate durable value.

The Sovereign Share

One of Roger’s most provocative ideas is the “sovereign share.”

Take the gross net assets of a country and divide it by the total population. What you get is a kind of citizen equity value, the implied share of national wealth each person inherits.

It is not a literal brokerage account. It is a way of thinking.

What is each citizen’s stake in the national balance sheet?

Are we passing on more equity to the next generation than we inherited?

Or are we consuming the asset base and calling it growth?

This reframes politics, investing, citizenship, and public finance. It turns arguments about spending, tax cuts, infrastructure, education, resource extraction, healthcare, and deficits into balance sheet questions.

Will this decision increase the sovereign share?

Will it reduce it?

Will it compound the next generation’s inheritance?

Or will it leave them with more liabilities and fewer assets?

That is a better question than whether this quarter’s GDP looked good.

AI and the Balance Sheet Shock

The conversation then moves into AI, where Roger’s framework becomes even more urgent. In most advanced economies, human capital is the largest asset on the national balance sheet. People’s knowledge, skills, productivity, creativity, and labor capacity drive enormous value. But AI creates a new uncertainty.

If intelligence becomes abundant, what happens to the value of certain forms of human capital?

Roger is careful here. In prior technological revolutions, jobs changed, but total employment often adapted over time. New roles emerged. Humans moved from hands to machines, from fields to factories, from factories to services, from routine labor to knowledge work.

But AI may be different because it moves into the cognitive layer. The machine is not merely replacing muscle. It is beginning to augment or replace parts of the brain.

If new, productive work emerges fast enough, human capital may adapt again. If not, the value of human capital on national balance sheets could shrink. That would be a profound economic, social, and political event.

And GDP may not warn us early enough.

That is why a balance sheet framework matters. It can help us ask not just whether AI companies are growing, but what AI is doing to the value of human capability across the broader economy.

The Governance Question Becomes Everything

Chris makes an observation in the conversation that brings the whole framework into focus. Every place has some natural resources or potential resources. Every place has some infrastructure or the possibility of building it. Every place has people. Intellectual capital is now being democratized through AI in ways that were unimaginable just a few years ago.

So what becomes the linchpin?

Governance.

Roger agrees.

If governance squanders the other assets, it does not matter how rich the natural resource base is. It does not matter how educated the population is. It does not matter how much infrastructure gets built. It does not matter how many patents exist or how much money flows through the system.

Bad governance can eat the balance sheet. Good governance can compound it. That applies to countries, states, cities, businesses, and families.

It is not partisan. It is structural.

Do the rules protect compounding?

Do leaders steward assets for the future?

Can temporary wealth be converted into permanent capital?

Can human capital be developed and deployed productively?

Can infrastructure be maintained rather than merely announced?

Can natural resources be converted into enduring assets rather than consumed and forgotten?

Those are the governance questions that matter.

The Ledger for Families and Business Owners

Near the end of the conversation, Roger brings the framework home.

Anyone who has built or sold a business intuitively understands the difference between the income statement and balance sheet. Revenue matters. Profit matters. Cash flow matters. But the real value is in what compounds.

If a business earns a lot and spends everything, it may look successful but fail to build enterprise value. If a family earns a lot and consumes everything, it may enjoy a high-status lifestyle but remain fragile. If a country produces activity but destroys its natural assets, underinvests in people, depletes infrastructure, and piles up liabilities, it may look prosperous while weakening.

This is why the framework is not only for macro nerds. It is for anyone who wants to preserve and grow wealth. Your personal income statement is what you earn and spend.

Your balance sheet is what remains, what compounds, what protects you, and what gives future options to the people you love.

Roger’s final point is human. Health may be the most important asset of all. In the United States, even a family with several million dollars of net worth can face devastation from a severe medical event. In other countries, that same risk may be structurally different. Asset protection depends on what the asset is, where it sits, and what system surrounds it.

That is the ledger again.

Not just money.

Assets, liabilities, governance, and fragility.

Closing Thought

This ATOMIQ LEVEL conversation with Roger Ohan is a rare kind of macro conversation because it does not get trapped in the usual debate about whether GDP is up, inflation is down, markets are strong, or politicians are winning.

It asks a more fundamental question.

Are we actually getting wealthier?

Roger’s answer is that we cannot know unless we look at the balance sheet. We need to know what is happening to natural assets, infrastructure, human capital, intellectual capital, financial assets, liabilities, and governance. We need to know whether we are compounding value or merely generating activity. We need to know whether the sovereign share is rising or falling.

For investors, this is a framework for seeing through headline noise.

For business owners, it is a reminder that cash flow without compounding can still lead to fragility.

For families, it is a reminder that high income is not the same thing as durable wealth.

For citizens, it is a reminder that the promises made in your name are liabilities on someone’s balance sheet.

And for leaders, it is a reminder that stewardship is not measured by how much activity you create today.

It is measured by what remains tomorrow.

Press play on this episode with Roger Ohan, if you want to understand why GDP alone is not enough, why governance may be the ultimate multiplier, and why the real wealth of a nation, a business, or a family lives on the balance sheet.

Because the income statement tells you what happened. The ledger tells you what (and who) survives.

The real risk is doing nothing!

~Chris J Snook

Thank you to everyone who tuned into my live video! Join me for my next live video in the app.