A transcript unlocks clips, previews, and editing.

The Odd Ducks Who Find the Cracks in Consensus and Profit From It

Lakshmi Gadapathi of Unicus Research explains short selling, private credit, auto-sector stress, ETFs, and why the best investors learn to question the story before the data confirms the break.

Subscribe to Unicus Research on Substack and follow Lakshmi Gadapathi and her team’s work if you want a sharper lens on short ideas, private credit, private equity, auto-sector stress, capital-structure fragility, roll-up risk, and the places where consensus narratives may be hiding real weakness.

Lakshmi made it clear in our conversation that Unicus does not publish its institutional short ideas directly on Substack for compliance reasons. That matters. The Substack is not the same thing as the client-only research product. But it is still the best place to understand the way she and her team think, how they question consensus, and why their work is gaining attention from some of the sharpest people on the platform.

At minimum, follow her.

At maximum, become a founding member or paid subscriber if the work fits your process.

Disclaimer: This conversation is educational and should not be treated as personalized investment, legal, tax, or financial advice. Short selling is risky. Long investing is risky. Private credit is risky. ETFs are not magic. Your own due diligence still matters. Talk to your advisor.

The Odd Duck Who Built a Research Firm With Wi-Fi and Her Brain

I invited Lakshmi Gadapathi onto ATOMIQ LEVEL because the signal kept showing up in my feed.

Her work was being read by people I respect. Her name kept appearing around some of the sharpest corners of finance Substack. People who have done well as guests on this show, people I consider legitimately brilliant, were subscribing to her work. The rankings for her channel’s growth velocity on MarketStack were undeniably increasing.

That is usually enough for me to pull the thread.

When I asked her where Unicus Research came from, she did not give me a polished founder story. She did not posture. She did not try to make it sound bigger than it was at the beginning.

She said she started with “Wi-Fi and her brain”.

That line says more than most bios.

Lakshmi came from independent investment research and built Unicus by looking at things differently. That is not a slogan in her case. It is the operating system. Her team is not stacked with the predictable pedigree checklist. She described them as unique people, the kind who question the norm, unpack everything, and ask why something is the way it is before they accept that it has to be that way.

That instinct is the foundation of Unicus. It is also the foundation of a short seller. Not the caricature of one.

The real thing.

The person who looks at a beautiful story, an admired CEO, a popular product, a sector everyone wants to believe in, and says:

“Is it really, though?’

That became the invisible title of the episode for me.

A Quick Word From Our Ecosystem Brand Partner

Before we get into this conversation deeply with Lakshmi Gadapathi, I want to thank one of our Wealth Matters 3.0 ecosystem brand partners: PEBL.

PEBL is a company I personally use across my own portfolio companies and personal strategy because hiring abroad or remote should not require founders, operators, family offices, or distributed teams to spend months building employment infrastructure before they can bring great people into the business.

Hiring abroad or remote can take months when you do it on your own, but with PEBL you can hire in over 185 countries in minutes and have your new hire onboarded by Monday.

PEBL is normally $399 a month per employee — already a no-brainer for what you get — but right now there’s a limited-time offer on their site that makes it even easier to get started.

Early in the conversation, Lakshmi said something I had never heard phrased quite that way.

“Short sellers are born, not made".”

I have heard entrepreneurs are born, not made. I have heard leaders are born, not made.

But short sellers?

The more she explained it, the more it made sense.

A real short seller is not simply someone who dislikes companies, roots against success, or wants the world to break. That is the lazy version. Lakshmi was describing a temperament. A way of seeing. A willingness to be intellectually alone long enough for reality to catch up.

Short sellers, in her telling, are odd ducks. They know they cannot please everyone. They know their work will make some people angry.

They know that when they challenge a narrative, they may trigger people who have an emotional, financial, or professional identity tied to that narrative being true.

That is why the work is not just analytical. It is psychological. It requires emotional intelligence, humility, discipline, and the ability to separate conviction from attachment.

Conviction based on facts is useful. Falling in love with your own idea is dangerous.

That distinction became one of the most important threads in the episode.

Entrepreneurs and Short Sellers Are Two Sides of the Same Coin

As Lakshmi unpacked the short seller’s mind, I could not help but hear the mirror image of the entrepreneur.

The entrepreneur is convinced about what the world can become.

The short seller is convicted about where the story does not hold.

The entrepreneur says, “This will be true because I am going to build it.”

The short seller says, “That may be the story, but here is the gap.”

Both can be lonely. Both can be misunderstood. Both can be early. Both can look wrong for a long time before they are proven right. Both can also be destroyed by their ego.

That is the part people miss. The great entrepreneur can lose the company by refusing to adapt. The great short seller can lose the trade by refusing to admit that timing, liquidity, politics, cult dynamics, or capital markets are more powerful than the thesis.

Lakshmi’s team tries to protect against that by building dissent into the process.

Her people push back. They do not exist to validate her. They exist to make the work harder to fool.

That is not easy. She admitted pushback can hit the ego. But ego is exactly the thing that can decimate a long or a short.

You can be right and still lose money. In markets, that is not a philosophical inconvenience. That is the whole game.

Three favors before you continue.

Hit the ❤️. The algorithm is a validation machine that needs your cheap dopamine to keep us in the top of your feed.

Hit the 🔄 restack. Somebody’s life will change passively today and you can get the credit for bringing it to them from both us and them.

Hit 📤 share. You know exactly one person in your email list or text stream who needs something on their playlist or reading wire today.

Drop a comment. Tell me your war story, your related triumph, or your biggest unanswered concern. I reply to the ones that make me laugh, cry, make me think, or make me money. Preferably all of the above.

One of the reasons I appreciated Lakshmi’s candor is that she does not romanticize being right. She talked openly about why Unicus avoids certain shorts, even when the thesis may look compelling on paper.

Carvana. Tesla. Cult stocks. Pharmaceuticals. Companies where the balance sheet may not be the only battlefield.

Her point was not that these names are good or bad in some absolute sense. It was that the question is never only, “Is the thesis right?”

The better question is:

Is this the hill you want to die on?

That is a very different filter.

A cult short may be fundamentally obvious in an idealized world. But markets do not operate in idealized worlds. They operate in real worlds full of charismatic founders, retail belief, legal budgets, lobbying, political connections, financing windows, momentum traders, passive flows, index inclusion, and people willing to stay irrational longer than your capital can stay alive.

Lakshmi does not want to be short a religion.

She wants a company-specific catalyst.

Lower cash.

No organic growth.

Higher debt.

A roll-up running out of acquisition math.

A business whose growth anniversary is about to expose what was temporarily hidden by acquired revenue.

A capital structure that can no longer hide behind the narrative.

That is the pragmatic short. Not activist theater. Not a moral crusade. Not “I am right, and the world must reorganize itself tomorrow so I can get rich.”

It is a trade with a path, and the “trade-off” is clear and acceptable.

Why They Wait for the M&A Anniversary

One of the most practical pieces of the conversation came when Lakshmi described how Unicus looks at roll-ups.

A company can buy growth. For a while.

When a company acquires another business, it may show revenue accretion for several quarters. The headline numbers can look stronger because the acquired revenue is now inside the consolidated financials. That does not mean the core business is healthy. It may just mean the company bought time.

Lakshmi said they wait for the anniversary of the M&A. That is when the comparison gets harder. That is when inorganic growth stops flattering the year-over-year numbers.

That is when the market may begin to see whether the company is actually growing or merely rolling forward on borrowed momentum. This is the kind of detail I love because it is not theoretical. It is a process.

The difference between a sharp observation and a tradeable framework is often timing. Unicus does not want to pick every penny off the floor. They are willing to leave money on the table.

That may be the most mature sentence in short selling.

The Auto Sector as a Live Case Study

We spent a meaningful part of the conversation inside the auto sector because it is one of those places where the lived signal and the official narrative do not seem to line up.

I shared my own recent experience buying a used 2011 BMW 5 Series for under $12,000 from two young operators in Grover Beach who had built a lean used-car dealership around reliable German and Japanese cars under $25,000. Their warehouse would not impress anyone. Their customer experience did. (original story here)

They had built an AI-powered dealer management system. They had an agent selling cars without the traditional dealership grind, bringing customers in for a very human-centric transactional and pickup experience with the owners of the dealership.

They were turning inventory fast and disciplined in their inventory load.

Then I compared that to the large dealer lots nearby, with hundreds of used cars, expensive real estate, financing pressure, trade-ins losing value, and a business model that still seems built around wearing customers down for hours over a monthly payment.

In my mind, the question was obvious:

How could you be long the traditional auto retail model right now?

Lakshmi did not flinch.

She believes the auto sector is effectively done in its current form. Not gone tomorrow. Not instantly collapse. But structurally changing. The old dealer-centric model is under pressure from online buying behavior, used-car platforms, inventory realities, affordability strain, and the fact that consumers do not want the old five-hour dealership ritual anymore.

People still need cars. The number of cars on the road is not going to zero.

But the business model that controls how those cars are sold, financed, priced, and moved may be entering a very different chapter.

That is where the short seller’s brain lives.

Not “cars are dead.”

More precise:

Which business model breaks when the consumer, financing environment, inventory cycle, technology layer, and price reality all shift at once?

The Mortgage 2.0 Feeling

I also shared a cigar conversation with someone involved in dealer finance earlier this week, serendipitously, who told me the paper was fine, that dealerships were moving loans at record rates, that people were taking on more $1,000 monthly car payments than ever in his career.

My reaction was visceral. It felt like Mortgage 2.0. Not because auto loans are exactly mortgages. Not because every dealership is a subprime lender. Not because the outcome must be identical.

But because the same emotional structure was there: a person making money pushing debt who could not see why the payment regime might not last.

Everyone needs a house. Until they cannot afford it. Everyone needs a car. Until the payment breaks the household.

That does not automatically tell you the trade. That is why someone like Lakshmi matters. The signal is not enough. You still need the structure, the company, the catalyst, the liquidity, the financing chain, the balance sheet, and the timing.

But the signal is where the questioning begins.

Is the paper really fine?

Are the consumers really fine?

Are the dealers really fine?

Is the inventory really worth what the balance sheet says?

Is the financing really durable?

Is the collateral really where the lender thinks it is?

Is it really, though?

Why Lakshmi Does Not Love ETFs

One of the audience questions pushed into a practical issue for investors who are mostly long public markets. If there are so many short themes and structural cracks, is there an ETF or public-market vehicle that captures them?

Lakshmi’s answer was direct. She does not like ETFs.

Not because ETFs are always bad. Because she wants to know what is inside what she owns.

In her view, an ETF may have a few attractive names at the top and a pile of things underneath that do not fit the investor’s real thesis. The top five may pull the whole thing up. The rest may be baggage.

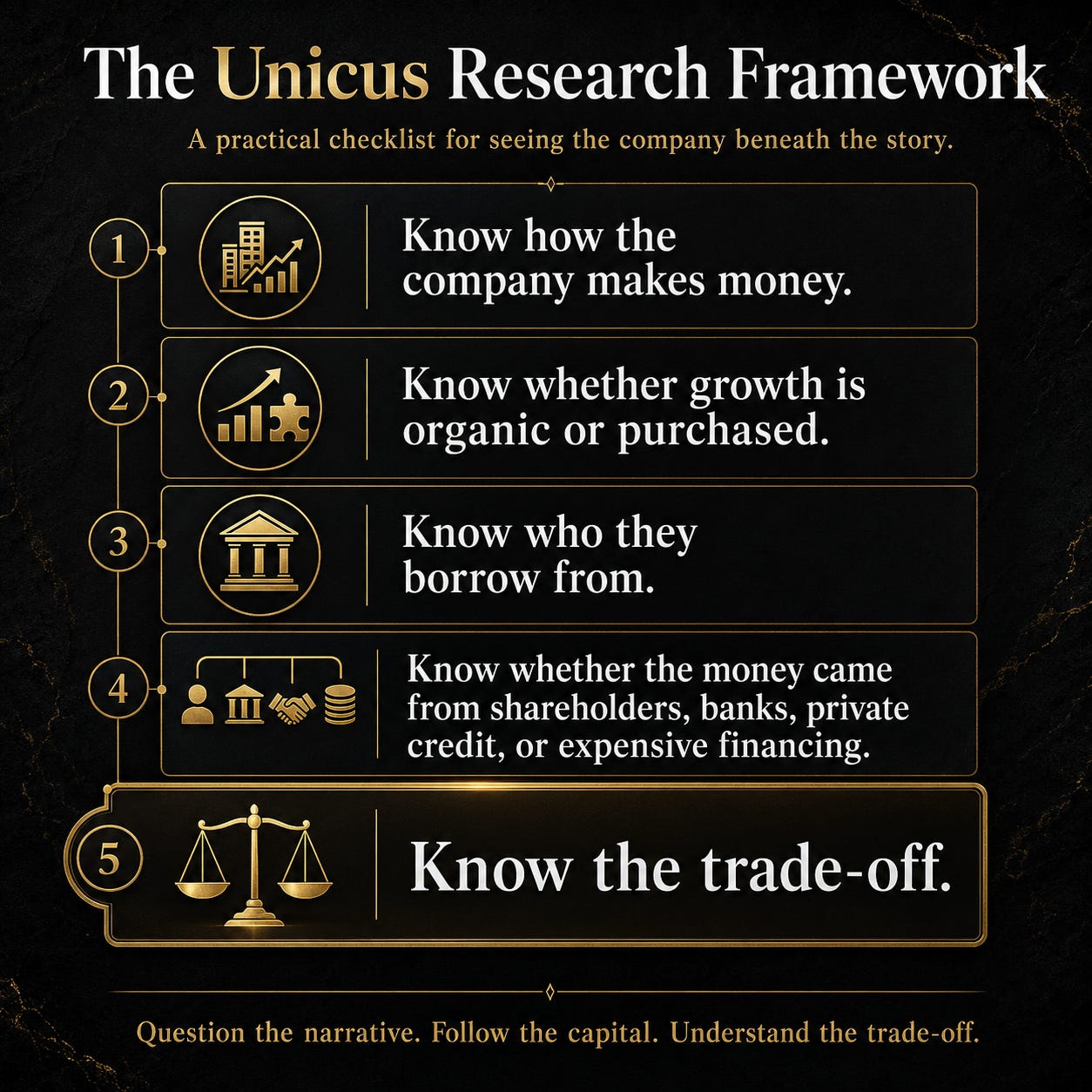

Her framework is brutally simple:

Know how the company makes money.

Know whether growth is organic or purchased.

Know who they borrow from.

Know whether the money came from shareholders, banks, private credit, or expensive financing.

Know the trade-off.

Everything in life has a trade-off. Every investment has a price.

That does not mean every investor has to abandon funds, models, or diversification. But it does mean investors should stop pretending wrapper names are the same as understanding.

An ETF is a container. She believes you should understand exactly what is inside the container.

What Is the Trade? What Is the Trade-Off?

This may be the most useful takeaway from the entire episode.

Ask two questions.

What is the trade?

What is the trade-off?

That applies whether you are a hedge fund manager, wealth advisor, family office, business owner, or regular investor trying not to get shoved into something you do not understand.

If the investment is liquid and boring but consistent, that is one trade-off.

If the investment is illiquid, fancy, higher-yielding, opaque, and locked up, that is another.

If someone tells you it pays more, ask “why?”.

If someone tells you it is safe, ask “compared to what?”

If someone tells you there is urgency, take 24 hours.

Lakshmi’s warning to retail investors was one of the plainest moments in the conversation. If someone is creating urgency around an investment, pause. The pressure is often part of how people end up in things they do not understand.

You worked hard for your money. Ask more questions before handing it over. That advice may sound basic. It is not basic when the room is full of confident people, shiny decks, acronyms, projected returns, and the subtle fear that everyone else is getting rich while you are asking annoying questions.

Be annoying. Your capital deserves it.

Private Credit, Shadow Banks, and the Data Hiding in Plain Sight

Lakshmi and her team have been mapping private credit and private equity exposure because, in her words, parts of the system look like a house of cards.

That theme fits directly into a larger Wealth Matters 3.0 concern.

After 2008, tighter regulation pushed a lot of lending activity outside the traditional banking system. Shadow banks and private lenders served a real purpose. They provided capital to borrowers and businesses that could not always get it through banks.

Then 2020 happened. Stimulus flooded the economy. Certain payments were paused. Credit lines expanded. Evictions were delayed. Student loan reporting and other pressures were altered. Consumers paid down debt, improved FICO scores, bought cars, extended themselves, and entered a different financing reality.

Now the lags are catching up. Tariffs. Energy costs. Geopolitical stress. Private credit. Auto loans. Consumer pressure. Roll-ups. Expensive debt.

Everything is layered on top of everything else with very little breathing room between shocks.

Lakshmi’s point is that the data is often there. People ask where Unicus gets it. Her answer is almost maddeningly simple:

It is right there at your fingertips.

But having access to data is not the same as knowing what to ask of it. That is the difference between information and intelligent research.

One of the reasons Unicus has built conviction in areas like auto is that they do not simply rely on polished industry data from the obvious sources.

Lakshmi made a point about Mannheim and other published data sources. She does not want to rely only on data that may be connected to the same industry incentives she is trying to analyze.

So they call people. Wholesalers. Dealers. Auction houses. Operators. Primary sources.

That kind of work is slower, messier, and less scalable than buying a data feed and pretending it tells the whole truth. It is also often where the signal lives.

The spreadsheet may tell you the price. The human operator tells you whether the bid is real.

The official report may tell you the inventory. The dealer tells you what is not moving.

The model may tell you the losses. The auction source tells you where the collateral actually went.

This is where Lakshmi’s team earns the name Unicus. They are not looking for consensus validation. They are looking for the part of the story the consensus has not priced yet.

The Product Lakshmi Is Building Next

Near the end of the conversation, we talked about where Unicus could go as a product.

I asked whether she was thinking about leveraging AI, MCP, APIs, or some kind of licensed feed so that their research and mapping could integrate into someone else’s product, especially for fiduciaries trying to understand exposure across private credit and private equity.

Her answer was yes.

Unicus is working toward an infrastructure that maps the universe of private credit and private equity, overlays it with their research, and eventually licenses that intellectual-property-protected infrastructure for a fee.

That matters.

Because the next generation of fiduciary work is not going to be only about asset allocation. It is going to be about exposure intelligence.

Where is the risk?

Who owns it?

Who financed it?

Who rolled it up?

Who marked it?

Who lent against it?

Who is exposed through a fund, a tranche, an SPV, a note, an ETF, a model portfolio, or a private placement?

Where is the money actually sitting?

That final question is going to define a lot of the next decade.

Where Is Your Money?

The phrase I kept coming back to during the episode was simple:

Where is it?

If a client owns SpaceX, where is it?

Direct shares? SPV? Fund? Secondaries platform? Wrapped inside something else?

If a client owns Bitcoin, where is it?

Cold storage with private keys? Exchange custody? ETF? Trust? Fund?

If a client owns private credit, where is it?

Direct loan? Interval fund? BDC? CLO? Feeder? Model portfolio? Insurance wrapper?

The answer matters. Because where it is often determines what it is. Investors love naming the asset.

They spend less time understanding the container.

That is where many risks hide. Lakshmi’s work is a reminder that the wrapper is not a footnote. The wrapper can change the risk profile entirely.

The Optimism of a Short Seller

As we began to wind down, I asked Lakshmi what had her excited about the future.

It felt almost contradictory to ask a short seller that question. Her job is to look at what is not right, what is not ethical, what is not working, what is overvalued, and what may be fragile.

But real short sellers are not pessimists. They are reality optimists.

They believe truth eventually matters.

They believe bad structures eventually reveal themselves.

They believe capital can be protected by asking better questions.

They believe information is abundant enough now that people can learn more, see more, test more, and push harder than they could when knowledge was locked away.

What excites Lakshmi is the amount of information available. But abundance cuts both ways. There is information. There is misinformation. There is data. There is noise. There are sources. There are incentives. There are headlines. There are angles.

Her advice was not “read more” in the shallow sense. It was read with a critical eye.

Ask what is missing.

Question the source.

Question her.

Question her team.

Question the person selling you the investment.

Question the urgency.

Question the product.

Question the wrapper.

Question the trade.

Question the trade-off.

The short seller’s gift is not cynicism. It is disciplined doubt.

Why You Should Press Play

Press play if you want to understand why short selling is not merely betting against a company, but a way of seeing gaps between narrative, capital structure, timing, and reality.

Press play if you want to hear why Lakshmi believes short sellers are born, not made.

Press play if you want to understand why Unicus avoids cult shorts, crowded 52-week-high momentum fights, pharmaceuticals, and anything where the ideal thesis may be overwhelmed by real-world politics, liquidity, lobbying, or personality.

Press play if you care about private credit.

Press play if you are a wealth advisor who has clients in opaque products and wants to sharpen your questions before the next liquidity event teaches the lesson for you.

Press play if you are a long-only investor who uses ETFs and model portfolios but wants to think more deeply about what is actually inside the wrapper.

Press play if you want to understand why the auto sector may be one of the clearest live case studies in consumer pressure, financing risk, business-model disruption, and dealership fragility.

Press play if you want to learn how an odd-duck team thinks.

And press play if you have ever heard a market story and felt the little voice in your head whisper:

Is it really, though?

Lakshmi Gadapathi is not trying to be liked by the narrative. That is why I enjoyed the conversation. She is direct, sometimes blunt, occasionally uncomfortable, and deeply practical. She is not interested in sounding like every other research shop. She is not packaging consensus in fancier language. She is not pretending that conviction is enough without timing, humility, and an understanding of the real-world forces that can keep a broken story alive longer than expected.

Unicus Research was built by odd ducks. That may be the point.

The world does not need more people who accept the deck because the logo looks impressive.

It needs more people willing to ask where the money is, how the company makes it, who lent it, what happens when the acquired growth anniversaries, where the collateral sits, whether the wrapper changes the asset, and what trade-off is being quietly accepted in exchange for yield, access, or story.

That is not cynicism. That is stewardship. Subscribe to Lakshmi Gadapathi and Unicus Research on Substack. Then press play on the full ATOMIQ LEVEL conversation. Because the real risk is not asking the uncomfortable question.

The real risk is doing nothing.

~Chris J Snook

Thank you TomD, Jon from Texas, and many others for tuning into my live video with Unicus Research! Join me for my next live video in the app.

Get more from Chris J Snook in the Substack app

Available for iOS and Android

Discussion about this video

THE ATOMIQ LEVEL

The show that rehumanizes wealth management for clients and advisors—decoding the matters of wealth one insightful conversation at a time—so you can grow and protect both your net worth and net happiness.

For the advisors, investors, and families mastering business growth, estate protection, and alternative assets like Bitcoin and private deals—all while staying sane, compliant, and fulfilled.

The mission: NetWorth + Net Happiness rising together as we navigate the next world order.

The show that rehumanizes wealth management for clients and advisors—decoding the matters of wealth one insightful conversation at a time—so you can grow and protect both your net worth and net happiness.

For the advisors, investors, and families mastering business growth, estate protection, and alternative assets like Bitcoin and private deals—all while staying sane, compliant, and fulfilled.

The mission: NetWorth + Net Happiness rising together as we navigate the next world order.