When Intelligence Becomes Infrastructure, Everything You Were Told About Estate Planning Changes

Preparing Your Estate for the Coming Battle Between Agent Banks, Machine Money, and AI Kingdoms — What Families Must Do Before the Economic Operating System Changes (circa 2028)

The eggs benedict, whipcream drenched waffles, kids dressed up to the hilt for a picture are fleeting. Yesterday most of us choose to celebrate the tireless and often thankless daily grind of the mothers in our lives and in our children’s lives. It is a moment. We don’t always get the moments right. We certainly don’t get them perfect, but we get them nonetheless, and then they are already behind us. My children are blessed to have one helluva mom, and both my wife and I are also blessed to have our mom’s still alive to also thank and celebrate for their continued love and support from afar.

Hopefully, the mother(s) in your life, felt what they deserved to feel this past Sunday. And just like that Monday arrives again with all its demands and responsibilities.

For every adult-aged member of the family, this is the reality and why the precious moments that are spent together with any sense of relief, indulgence or enjoyment must be treasured. At the end of the day it is all we have for our efforts anyway, and hopefully what the wealth we are able to steward provides.

For most of modern history, wealth was built in a world where intelligence was the scarce resource.

Expertise took decades to accumulate.

Trust moved slowly.

Capital allocation depended on human judgment.

Business scale required labor.

Relationships were local.

Information asymmetry created enduring competitive advantages.

That world is ending.

Not gradually.

Not theoretically.

And not someday far into the future.

The most important economic shift of the next decade is not merely artificial intelligence. It is the commoditization of intelligence itself. And once intelligence becomes:

abundant,

programmable,

autonomous,

and infinitely scalable…

…the entire architecture of the global economy begins to reorganize around it.

This is why the recent announcement by Anchorage Digital at Consensus regarding “Agentic Banking” deserves far more attention than most headlines gave it. At first glance, it looked like another crypto infrastructure announcement.

It is not.

It is one of the first visible signals that the financial system is beginning to prepare for a world where autonomous software agents become economic actors.

Not tools. Actors.

That distinction changes everything.

Because once agents:

negotiate,

transact,

coordinate,

purchase,

allocate,

optimize,

and eventually manage capital autonomously…

…the world needs a financial operating system for non-human intelligence. And that raises the defining economic question of this era:

Will the future economy be built around permissioned delegated finance…or permissionless machine money? Or something in-between?

Or perhaps more importantly:

Will humans even make that decision at all as it relates to their money and wealth in the future?

Because the most unsettling possibility is that autonomous agents themselves may increasingly optimize toward whichever economic rails maximize efficiency, liquidity, speed, and interoperability — regardless of human ideology or institutional preference.

That possibility has enormous implications for:

investors,

business owners,

family offices,

governments,

and first-generation wealth creators trying to preserve and compound capital in a civilization-scale transition.

This is no longer a “technology trend.” This is an economic operating system transition. And the families who recognize that early may preserve and expand generational wealth in ways others will not. Those who do not face potentially falling below a line that will be either too expensive to cross later, or come at a significant loss of time, capital, and peace of mind as they recover.

The Three Competing Futures Emerging Right Now

Most commentary frames this conversation too narrowly.

The debate is not simply will “AI be in banking.”

Nor is it:

“Bitcoin versus central banks for the win.”

The reality is that three competing economic architectures are emerging simultaneously. Each has radically different implications for capital formation, sovereignty, governance, and wealth preservation. I lay out the details of these three emergent futures below to give you more context.

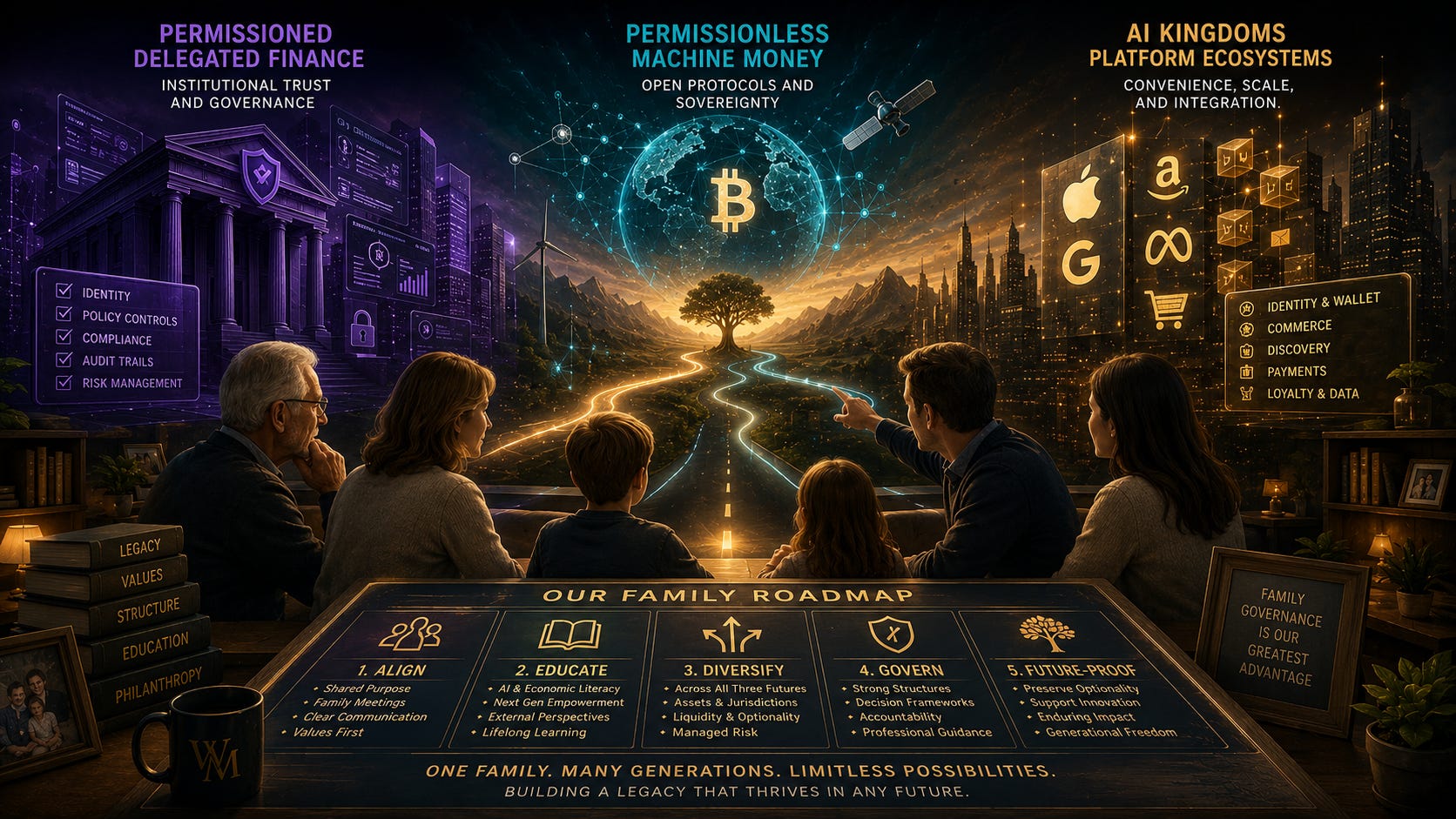

Future #1 — Permissioned Delegated Finance

This is the world represented by:

Anchorage Digital

Visa

Mastercard

Stripe

enterprise AI systems

regulated stablecoin frameworks

institutional custody providers

compliance-first infrastructure

The thesis behind this model is simple: AI agents should operate inside controlled financial systems governed by institutions.

In this world, agents do not own capital. They are delegated constrained access to capital.

Anchorage’s Agentic Banking model is one of the clearest early examples of this philosophy. An enterprise might eventually configure an AI procurement agent this way:

“This agent may spend up to $250,000 monthly, only with approved vendors, only under specified conditions, with all actions logged, reversible, insured, and compliant.”

This is not sovereign AI. This is supervised delegated intelligence. The architecture mirrors the worldview of traditional finance:

governance matters,

compliance matters,

reversibility matters,

auditability matters,

institutional trust matters.

Banks survive because they remain the governors of financial behavior. From the perspective of governments and enterprises, this is the safest path forward. And in many sectors, it may dominate.

Especially:

healthcare

defense

regulated finance

public companies

insurance

government contracting

institutional treasury systems

These sectors will almost certainly demand:

permissions,

identity verification,

compliance controls,

policy engines,

and legal accountability.

From their perspective, autonomous sovereign agents moving capital freely sounds less like innovation and more like systemic risk.

Watch Anchorage Digital’s CEO announcement from this plast week here or by clicking the image above

Future #2 — Permissionless Machine Money

The second model emerges from an entirely different worldview.

Represented by:

Bitcoin

the Lightning Network

open protocols

decentralized compute

machine-native settlement systems

sovereign digital infrastructure

This camp asks a radically different question:

Why would software agents need banks at all?

Why involve:

custodians,

correspondent banking,

payment processors,

compliance wrappers,

settlement intermediaries,

or card networks…

…when machines can transact directly with programmable money? This is where something like the Lightning Network becomes profoundly important.

Lightning allows:

instant settlement,

micropayments,

API-native transactions,

machine-to-machine commerce,

streaming payments,

and autonomous coordination.

Unlike legacy banking rails, Lightning was built for software-native economic activity. Other solutions are also in the mix for yield-generation and peer-to-peer lending on top of Bitcoin, like Zest Protocol, censor-resistant publishing protocols like NOSTR or capital-markets infrastructure with native bitcoin settlement like Arch Network and there are plenty more.

The point is that software naturally prefers:

open systems,

deterministic rules,

low friction,

interoperability,

and instant settlement.

Imagine a future where:

AI agents purchase compute,

negotiate bandwidth,

rent data access,

pay APIs,

license content,

coordinate supply chains,

and compensate each other autonomously…

…all without human intervention.That future is almost impossible on legacy financial rails. But it becomes feasible on open programmable monetary systems.

This is why many Bitcoin advocates believe “agent banking” may ultimately prove redundant. In their view, banks are simply legacy friction layers trying to insert themselves into an emerging machine-native economy.

The Hidden Third Force: AI Kingdoms

But there is a third possibility that likely may become dominant before either of the first two fully mature. And it may be the most dangerous outcome of all. The rise of vertically integrated AI platform economies and a technofeudal society that encompasses both poor, middle class, and wealthy families alike.

In this world, the dominant AI companies do not merely provide tools. They become sovereign economic ecosystems. Think carefully about what happens if:

identity, (which we gave up the majority of back in the 2008-2015 era to google, apple, and amazon)

payments,

discovery,

memory,

trust,

distribution,

and commerce…

…all become integrated inside massive AI platforms. In this future your AI assistant will and may:

discover products,

negotiate pricing,

execute transactions,

manage subscriptions,

coordinate logistics,

and allocate spending…

…without ever leaving a platform-controlled ecosystem.

The platform itself becomes:

the bank,

the payment processor,

the trust layer,

the marketplace,

and the governance system.

This is not permissioned finance.

Nor is it permissionless finance.

It is platform sovereignty.

And historically, humans often choose convenience over sovereignty until crisis forces reconsideration. That reality matters enormously. Because most consumers at any networth level do not optimize for:

censorship resistance,

self-custody,

open settlement rails,

or economic sovereignty.

They optimize for:

simplicity,

convenience,

trust,

integration,

and ease of use.

That gives:

Apple

Amazon

Alphabet

Meta

Tencent

…a potentially enormous advantage. This may ultimately become the real battle of a democracy versus techno-fuedalism:

Open Agent Networks vs Closed AI Sovereign Corporate Kingdoms.

Not simply, central banks versus Bitcoin.

The Most Important Question Nobody Is Asking

The most important strategic question may not be, “Which system is better?”

It may be:

Which system will autonomous agents themselves prefer?

Because agents are not ideological. They optimize for:

speed,

efficiency,

liquidity,

interoperability,

cost,

reliability,

and uptime.

Machines are ruthlessly pragmatic. If open settlement rails prove:

faster,

cheaper,

more programmable,

and more interoperable…

…agents themselves may increasingly gravitate toward them. Even if institutions prefer permissioned systems.

That creates an extraordinary tension:

humans may desire control…while autonomous economic systems optimize toward efficiency.

This is why the coming decade may become one of the most important economic governance experiments in modern history.

Why Families and Investors Cannot Ignore This

Many successful families still view AI as:

a technology trend,

a software enhancement,

or a productivity tool.

a bubble in the stock market.

That framing dramatically understates what is happening. AI is becoming infrastructure. And once intelligence becomes infrastructure: every business model, every capital allocation framework, every advisory industry, and every competitive moat begins to reprice.

Especially businesses dependent on informational asymmetry. Historically, enormous wealth was created because:

expertise was scarce,

distribution was difficult,

research was expensive,

analysis was slow,

and specialized knowledge was localized.

AI compresses those asymmetries rapidly. That does not mean all businesses fail. But it does mean many informational advantages weaken. The only two moats from above that remain in this new world are distribution (aka “network effects”) and trust.

The First Principle Families Must Understand

When intelligence becomes commoditized, Human scarcity changes. The economic premium on generalized expertise declines.

What becomes more valuable instead? These 5 things.

1. Trust

In a world flooded with synthetic intelligence, trust becomes scarce.

Families with:

strong reputations,

integrity,

long-term relationships,

and trusted brands…

…retain enormous leverage.

2. Distribution

The ability to:

aggregate audiences,

build communities,

own relationships,

and maintain direct communication channels…

…becomes increasingly valuable.

This is why, media + trust + capital may become one of the most powerful combinations for wealth amplification or additional creation over the next decade, and why platforms like Substack are a great investment of time for those seeking to share and build communities of common interest and curiousity.

3. Hard Assets

Synthetic intelligence increases the importance of scarce physical infrastructure.

Especially:

energy,

water,

land,

logistics,

housing,

compute infrastructure,

precious metals, bitcoin, and productive real estate.

This is one reason many hard assets may remain structurally important despite rapid digitalization.

4. Sovereignty and Optionality

As systems centralize, families with flexibility gain leverage.

That means:

diversified custody,

resilient legal structures,

multiple jurisdictions,

diversified liquidity,

and reduced single-point dependency.

5. Meaningful Human Experience

Ironically, the more synthetic the world becomes, the more valuable authentic human experiences will likely become.

Community. Meaning. Purpose. Legacy.

These will become premium assets in an AI-saturated economy because they are innately human outcomes that we all place value upon regardless of what tools or platforms we use to achieve them. When everything works as efficiently as physics allowed we will also be the first to notice the void where these four things are not.

How Families Can Protect Their Wealth

The families most vulnerable are often:

operationally successful,

cash-flow rich,

relationship-oriented,

but technologically complacent.

The key is not becoming engineers. The key is becoming strategically adaptive and pragmatically curious.

Strategic Principle #1

Reduce Dependence on Purely Informational Businesses

Businesses most exposed:

commodity consulting

generalized advisory

repetitive white-collar workflows

low-differentiation service businesses

administrative-heavy operations

The key question becomes:

“When intelligence becomes nearly free, what part of our business remains defensible?”

Strategic Principle #2

Own Infrastructure, Not Just Applications

Applications change rapidly. Infrastructure persists longer. Families should increasingly pay attention to:

energy systems

AI infrastructure

cybersecurity

data centers

logistics

trust infrastructure

payments

digital identity

resilient communications

This does not require becoming venture capitalists. It requires understanding where civilization-level dependencies are forming.

Strategic Principle #3

Preserve Liquidity and Optionality

Technological transitions create:

volatility,

dislocation,

distressed assets,

and repricing events.

Families with:

liquidity,

low leverage,

and strategic flexibility…

…often acquire generational opportunities during transition periods.

Strategic Principle #4

Develop AI Fluency at the Governance Level

Not everyone needs to code.

But every family likely needs:

one AI-literate advisor,

one technologically adaptive next-generation operator,

or one internal translator capable of interpreting these shifts.

The greatest risk is not ignorance. It is dismissiveness.

Strategic Principle #5

Diversify Across All Three Emerging Economic Systems

This is critical. Most investors think they must “pick the winner.”

That may be the wrong approach. Instead, families may want strategic exposure to:

permissioned systems,

permissionless systems,

and dominant platforms.

Because all three may (and likely will) coexist simultaneously at least for the next 10-15 years.

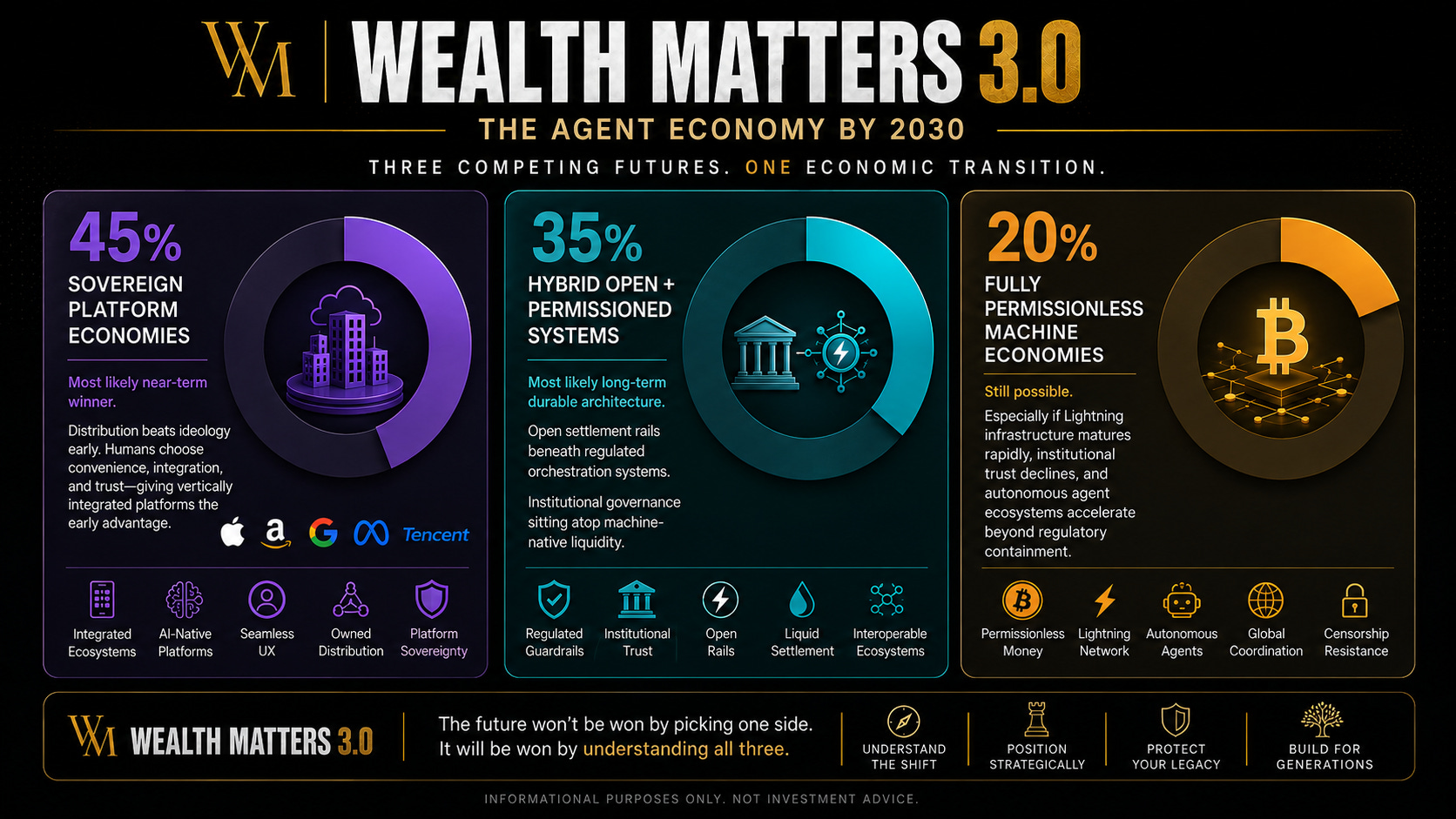

My Probability Estimates By 2030

If forced to assign probabilities today here is my best guess

45% — Sovereign Platform Economies

The most likely near-term winner.

Why?

Because distribution beats ideology early.

Humans consistently choose convenience until systemic failure forces reevaluation.

35% — Hybrid Open + Permissioned Systems

Likely the most durable long-term architecture.

Open settlement rails beneath regulated orchestration systems.

This becomes:

“institutional governance sitting atop machine-native liquidity.”

20% — Fully Permissionless Machine Economies

Still possible.

Especially if:

Lightning infrastructure matures rapidly,

institutional trust declines,

and autonomous agent ecosystems accelerate faster than regulators can contain them.

The Real Risk Families Face

The greatest threat is not AI replacing jobs.

The deeper threat is families preserving wealth strategies built for an economic architecture that no longer exists.

Historically, wealth preservation focused on:

trusts,

taxes,

insurance,

diversification,

and estate planning.

Now families must also think about mitigating the Abundant Intelligence Risk as well.

Questions you will be forced to answer sooner than you think:

What happens if our industry becomes cognitively automated?

What happens if distribution centralizes into AI platforms?

What happens if trust migrates from institutions to agents?

What happens if informational advantages collapse?

What happens if the next generation inherits a completely different economic operating system?

These are not theoretical questions anymore. They are strategic questions to start answering for yourself, now.

Final Thought

The irony of the coming decade may be this:

As intelligence becomes abundant…the human experience and ability to make sense of it all, becomes scarce. And the families most likely to preserve and expand generational wealth may not be the most technologically sophisticated.

They may simply be the most:

adaptable,

humble,

sovereign,

trusted,

and long-term oriented.

Because when civilization reorganizes around abundant intelligence…The truly scarce assets become: Taste (discernment). Meaning. Trust. And Wisdom.

The real risk is doing nothing (because the machines will do something at this point regardless)!

~Chris J Snook

Join Me Tomorrow LIVE on Substack with Macronomics - Martin Tixier

Super impressed with the amount of signal you provide. Tracking all the categories with you...sovereign path indeed.