There is a moment early in the conversation where Chris frames the entire open office hours episode theme as a contradiction in the Knowing vs Doing gap.

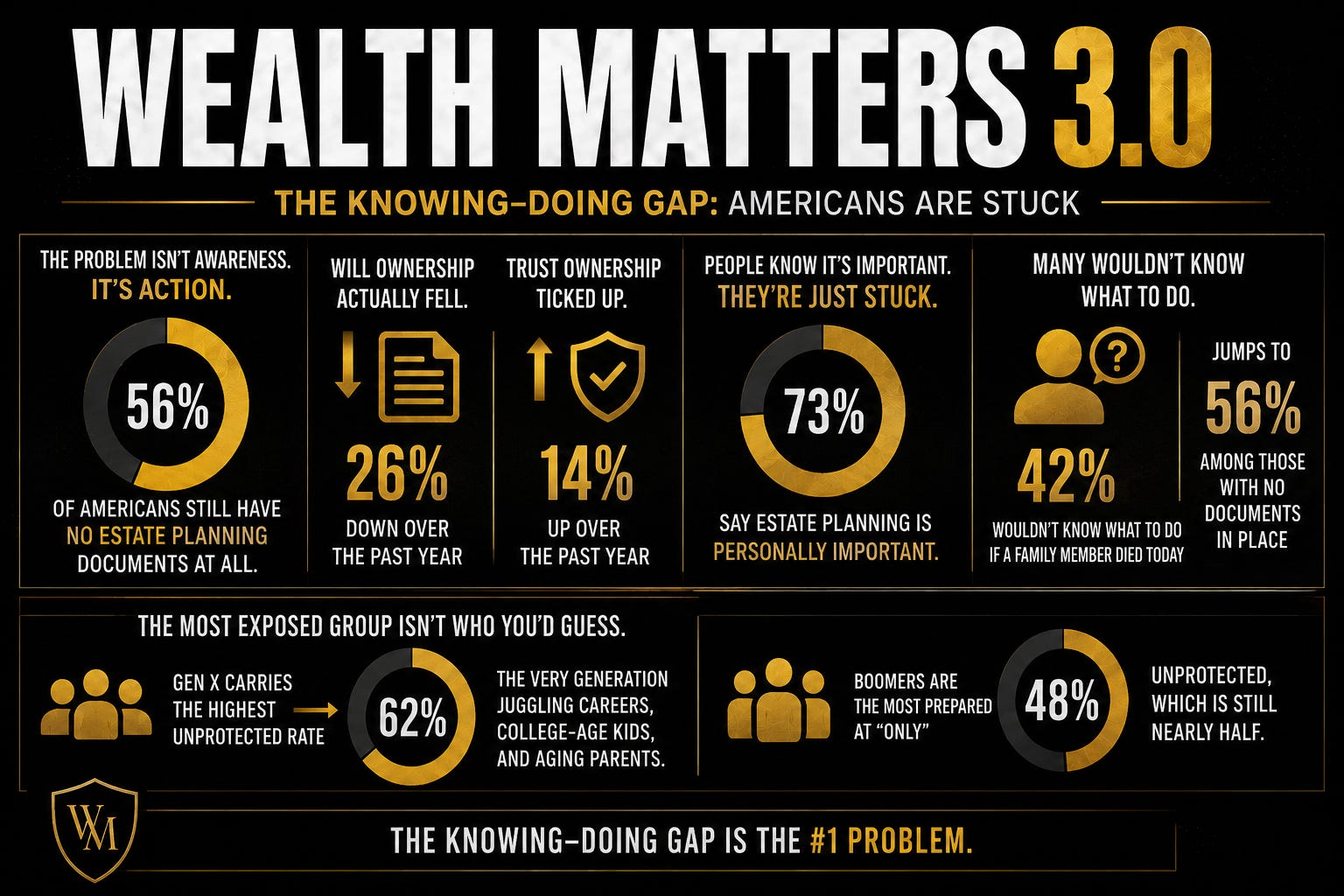

Americans over 50 know estate planning matters. They feel the anxiety. They see aging parents. They have kids, homes, retirement accounts, businesses, second marriages, prior marriages, blended families, passwords, insurance policies, healthcare decisions, and the slow realization that life is not as administratively simple as it used to be.

And yet many still have no basic documents in place.

Others have documents that are outdated.

Still others have documents that were created once, placed in a binder, and never reviewed again.

Meanwhile, the anxiety is often pointed at the wrong target. People worry about estate taxes, but the real risks are often more ordinary and more dangerous: no plan, stale documents, unfunded trusts, old beneficiary forms, long-term care costs, probate, family conflict, incapacity, digital lockout, and business succession that never got designed.

That is why Matt Chats exists.

Not to scare people.

To humanize the conversation before a crisis forces it.

Matt Meuli is not just a guest in this episode. He is Chris’s counsel, partner, and friend. That gives the conversation a different texture. It is not two people performing expertise at each other. It is one person asking the questions families actually ask when the camera is off, and another person answering from decades of experience helping clients navigate the uncomfortable intersection of law, money, mortality, family, control, and care.

Matt makes his disclaimer clear. This is not legal advice. His answers are educational. His opinions come from experience, but every family needs advice specific to its own situation.

Then he gets to work making the intimidating feel understandable.

Need to Talk?

Subscribe to Shields & Succession inside Wealth Matters 3.0 to stay alerted for future Matt Chats, live office hours, replays, and upcoming articles.

If at any point reading this (or listening/watching) you want to book a human one-on-one pre-consult with Matt Meuli’s team you can talk to an actual human M-F at the numbers below:

Clients in all 50 States and Territories Call: 307-463-3600

Colorado Residents Only Call: 970-820-0090

Call, ask the question, and start the conversation before the hospital, courthouse, nursing facility, creditor, or crisis starts it for you.

Your “Estate” Is Just “Your Stuff”

The first breakthrough in the episode is linguistic.

Matt says many people do not even know what an estate is. They hear the word and picture Downton Abbey, castles, massive land, family dynasties, tax lawyers, and the kind of wealth they do not believe they have.

That misunderstanding is expensive. An estate is not only a mansion.

An estate is your stuff. (Your condo. Your car.Your bank account. Your retirement plan. Your family photos. Your passwords. Your phone. Your business. Your house. Your insurance policy. Your digital life. Your medical decision-making authority. Your unfinished obligations.

Estate planning is simply the orderly movement and management of that stuff from one stage to the next, whether that means incapacity, death, care, guardianship, inheritance, business transition, or family continuity.

Once Matt reframes it that way, the whole subject becomes less abstract.

The question is no longer, “Am I wealthy enough to need an estate plan?”

The question is:

“Who gets to make decisions about my stuff and my life if I cannot?”

That is the question most families avoid or forget to ask, because they don’t own Downton Abbey.

It is also the question that determines whether grief becomes compounded with chaos.

You Already Have a Plan. You Just Won’t Like It.

One of the strongest points in the episode is Matt’s warning that doing nothing does not mean there is no plan.

There is always a plan.

If you do not write one, the state you live in provides one.

That default plan may decide who receives your property, who has priority, who can act, who inherits, who gets left out, and who has to go to court. In simple situations, the default may feel tolerable. In real families, it can become absurd quickly.

Matt gives examples that make the risk tangible. A married person without children may assume everything goes automatically to the spouse. Depending on the state, parents may receive a share. Suddenly, a surviving spouse may co-own a home with in-laws.

In a blended family, children from a prior relationship may inherit alongside a current spouse. If a child is still a minor, the ex-spouse may end up managing the child’s share, creating the kind of emotional and legal entanglement no one would have chosen on purpose.

That is the danger of relying on the plan you never read and certainly weren’t consulted with when it was designed.

The state does not know your family story. It only knows the statute.

The Legacy of Unanswered Questions

Chris brings the point home with a line that sits underneath the entire episode: the problems you leave behind become part of your legacy.

That is a hard truth, but it is not meant to shame anyone. It is meant to clarify. If your family has to fight through confusion while grieving, that becomes part of the story.

If your spouse has to negotiate with your parents, stepchildren, creditors, or the court, that becomes part of the story.

If nobody knows where your accounts are, what your passwords are, who your advisor is, or what your wishes were, that becomes part of the story.

If your children have to guess whether you wanted to be kept alive, where you wanted care, or who was supposed to make decisions, that becomes part of the story.

Estate planning is not only about assets. It is about not forcing the people you love to make impossible decisions without a map.

The Smartphone Problem

One of the most practical moments in the conversation comes when Chris shares a personal story.

His phone and laptop became unavailable for several hours during a day when he had meetings and obligations. Nobody died. Nobody was hospitalized. It was not a catastrophe. But for seven hours, he could not access his email, accounts, contacts, or two-factor authentication. He could not remember most phone numbers. He could not get into the systems that run modern life.

It was a temporary inconvenience that revealed a permanent vulnerability. This is the new estate planning frontier most families underestimate.

It is not only where the will is.

It is where the passwords are.

It is who can access the phone.

It is whether anyone knows the two-factor authentication path and has a duplicate copy of the Authenticator app for all the accounts.

It is whether someone can find the bank accounts, crypto wallets, insurance policies, subscriptions, bills, documents, advisors, and medical contacts.

Matt sharpens the point. Chris was alive, awake, and able to troubleshoot. Imagine if he had been unconscious on the beach.

That is why every person needs a champion.

Someone has to know where to look, who to call, and what authority they have.

Talking to Parents Without Making It Weird

The second major theme is the conversation many adult children dread.

How do you ask your parents about their estate plan without sounding like you are trying to get your inheritance early?

Matt’s answer is simple and powerful: lead with “help”.

Do not begin with, “What am I getting?”

Begin with, “What information do I need so I can help you?”

The conversation should be framed around care, not entitlement. Adult children can ask whether parents need help paying bills, organizing documents, managing appointments, understanding where things are kept, or making sure someone has the authority to step in if needed.

It is also important to acknowledge that parents may not want to disclose exact dollar amounts. They may not want their children to know everything. That does not mean the conversation is impossible. Matt explains that parents can share structure without sharing every number. They can explain who has authority, where documents are located, what the wishes are, and what happens if care is needed.

The point is not to invade privacy. The point is to prevent chaos.

The Sibling Problem

Family planning becomes even more complicated when siblings are involved.

One child may live nearby. Another may live across the country. One may be organized. Another may avoid conflict. One may be the natural caregiver. Another may be financially anxious. One may assume everything should be equal. Another may believe fairness should account for years of caregiving labor.

Matt tells a story that captures the issue. A parent puts a caregiving child on a joint bank account and repeatedly says the child should divide the money among siblings after death. During life, the caregiver agrees. But after years of changing diapers, managing care, missing work, giving up income, and carrying the burden while siblings visited only occasionally, the emotional math changes.

The account legally belongs to the caregiver. And the caregiver starts thinking, “I earned this.”

Maybe they did. Maybe they did not.

But the problem was not solved in writing before grief and resentment entered the room.

That is why communication and structure matter. A good plan does not rely on exhausted people making perfect decisions after someone dies.

Asset Protection, Estate Planning, and Legacy Planning Are Not the Same Thing

Another valuable part of the conversation is Matt’s distinction between estate planning, asset protection, and legacy planning.

Estate planning is the orderly transition of your stuff.

Asset protection asks how that stuff is protected from creditors, predators, lawsuits, divorces, care costs, taxes, or poor decisions, either while you are alive or after assets pass to beneficiaries.

Legacy planning asks what happens beyond the legal documents. It deals with values, stewardship, family continuity, business transition, and the kind of imprint you want to leave.

These categories overlap, but they are not identical.

A basic estate plan may avoid probate and move assets to the next generation. A stronger plan may also protect beneficiaries by keeping inherited assets in structures that are harder for creditors, ex-spouses, lawsuits, or bad decisions to reach.

For someone seeking asset protection during life, the planning path may be different. It may involve giving up some level of direct control, using trustees, or creating structures in jurisdictions that allow stronger creditor protection.

The key is intention.

You cannot build the right structure until you know what problem you are solving.

Probate Is a Public Process, Not a Private Family Matter

Matt’s explanation of probate is one of the most memorable parts of the episode.